Week 7 and 8: Labor Market Impacts of COVID-19 on Businesses: Update with Homebase Data Through May 23

- By

- May 29, 2020

- Rustandy Center for Social Sector Innovation

Week 1: Labor Market Impacts of COVID-19 on Hourly Workers in Small- and Medium-Sized

Businesses

Week 2: Update with Homebase Data Through April 11

Week 3 and 4: Update with Homebase Data Through April 25

Week 5 and 6: Update with Homebase Data Through May 9

Note: The results described in Figure 2 have been updated due to an error. Click here for the complete erratum. The error did not affect any of the other figures or results.

Below, we update our analysis of the labor market impacts of COVID-19 on small- and medium-sized businesses using Homebase time-card records through May 23.

The trends we identified in our last update continue. Notably, firms continue to reopen and mainly rehire those employed before the crisis. Below, we highlight a handful of new facts about the extent of these reopenings and which firms are more likely to reopen. Although some firms have reopened, we want to be clear that a recovery is far from complete. Almost one-third of firms in our baseline sample remain closed, and among the firms that ever shutdown, just over half remain closed. Of those that have opened, most are operating at a reduced scale.

We will update these facts frequently to track these patterns over time and add new information as the COVID-19 situation develops. An up-to-date version of this summary will be maintained here.

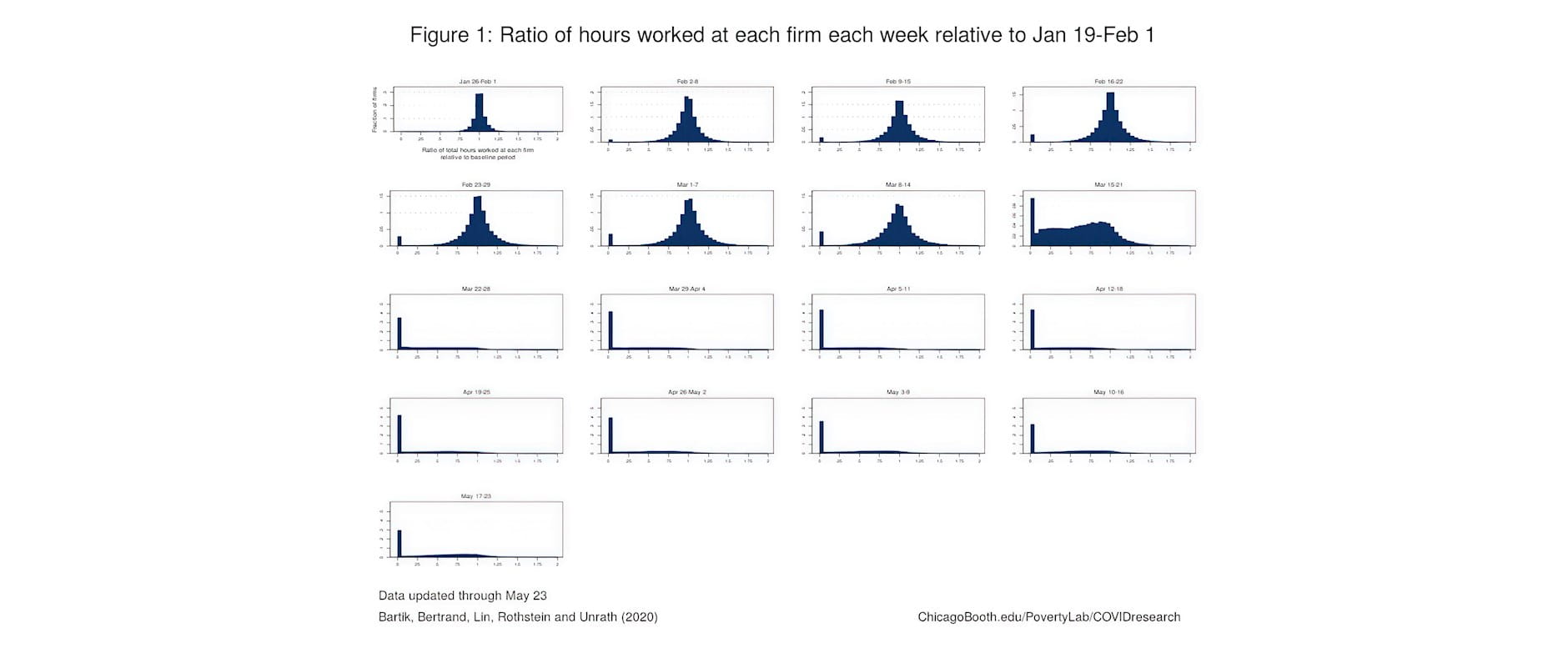

Fact #1: Firms continue to reopen and restore workers’ hours.

Thirty percent of firms from our baseline sample remain shut down, down from a high of 45 percent in the beginning of April (Figure 1). Of the firms that ever have shutdown, nearly half (44 percent) have now reopened and remained open through last week.

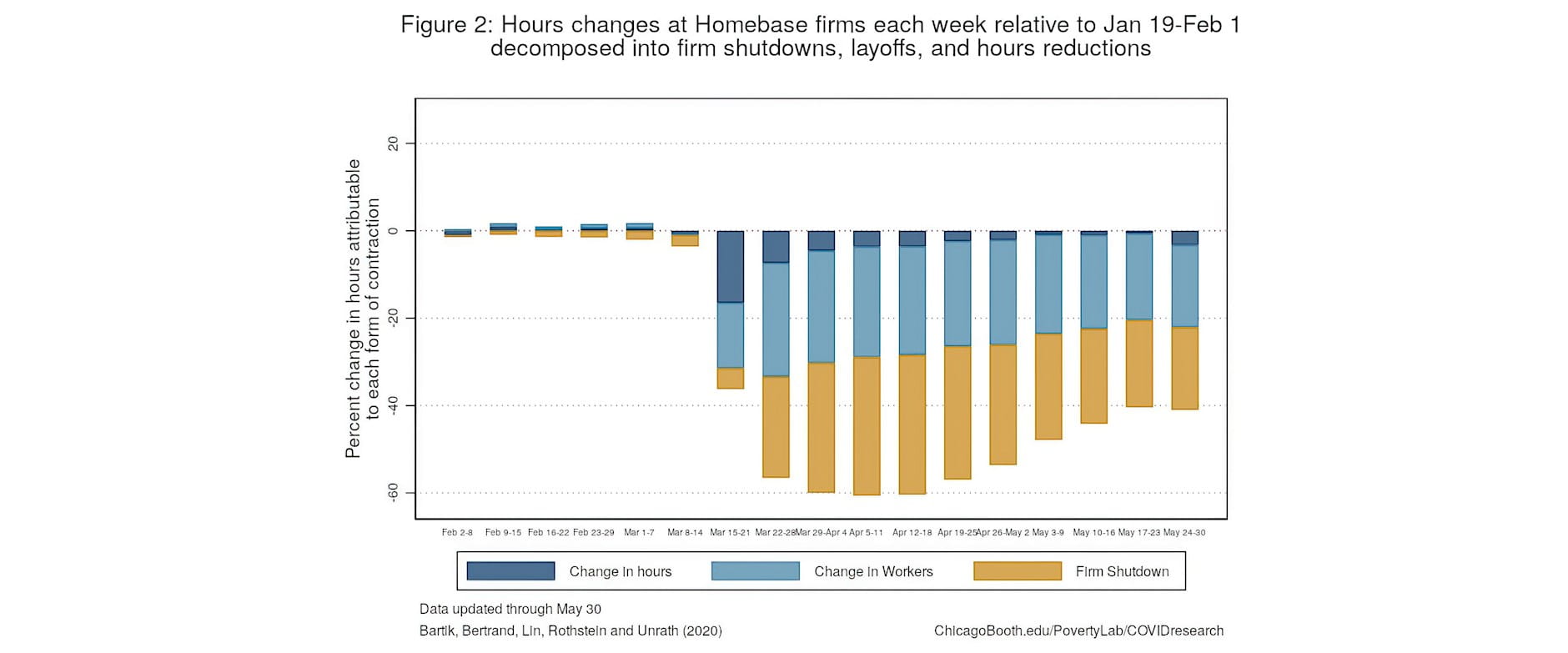

Hours worked last week were 32 percent lower than the average in our baseline period. That’s down from nearly 60 percent in mid-April (Figure 2). That recovery is mainly attributable to firms reopening. The share of hours lost due to firm closure declined from about 32 percent in mid-April

to 20 percent last week. The share lost due to layoffs fell from 25 percent in mid-April to about 20 percent last week.

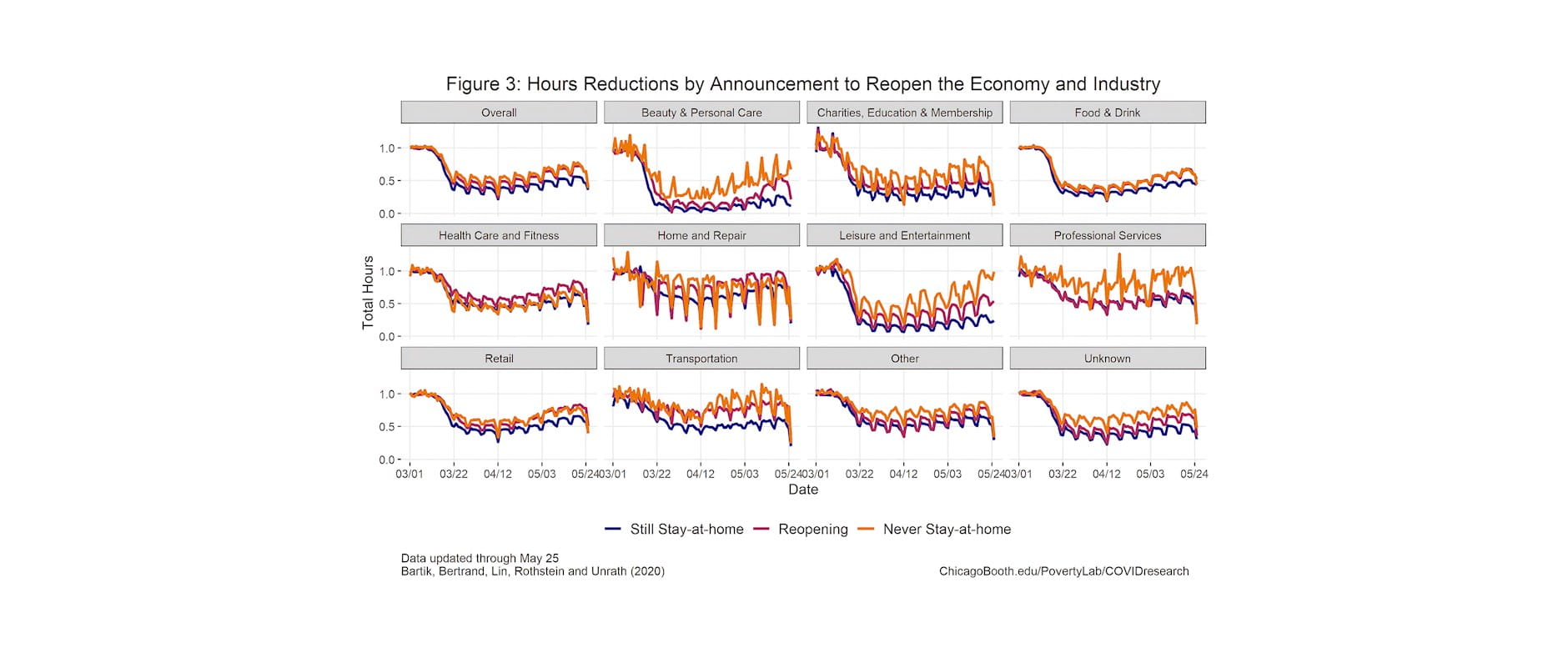

Fact #2: Firms in “reopened” states have restored the largest share of hours.

Hours also bounced back more in states that moved to reopen than in states that never shut down or remained shut down (Figure 3). In these “reopened” states, total hours in the past week (May 17-23) were 56 percent higher than their respective low. In states that remain shut down, hours were 47 percent higher, and in states that never closed businesses, hours are 40 percent higher.

We should note that these differences may not be the result of states’ decision to reopen or remain shut down. The likelihood of reopening is related to local disease burden and a number of other factors, which themselves are related to policymakers’ decisions about allowing firms to reopen. It’s also worth noting that, though there is a difference, the gap remains fairly limited. Government shutdowns of non-essential businesses do not appear to be the only obstacle to firms reopening.

There are notable industry differences as well. Hours at beauty and personal care firms and leisure and entertainment firms are 370 and 215 percent higher than their respective lows. Hours at transportation and professional services firms are only 20 percent higher than their lows.

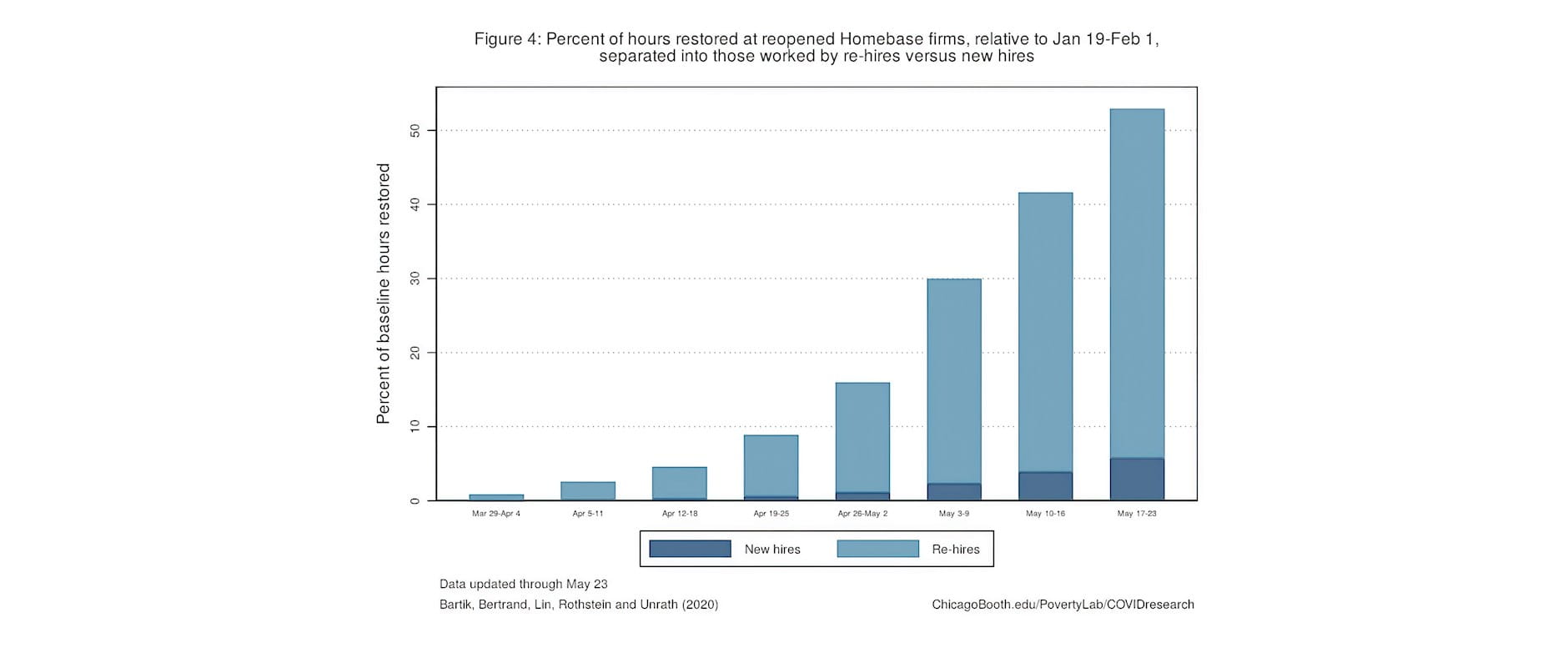

Fact #3: Reopened firms tended to rehire original employees, but they’ve only restored a portion of their original hours.

In Figure 4, we show how much these firms’ baseline hours and workforce were restored through each week. By last week, these reopened firms had collectively regained over half of their baseline hours and nearly 60 percent of their baseline employment levels. As in our last update, almost 90 percent of this reemployment came through rehiring employees who worked at the firms before they shut down, as opposed to new hires. This suggests that, so far, most worker-firm matches at these firms have been maintained through the crisis, firm closures, and reopenings.

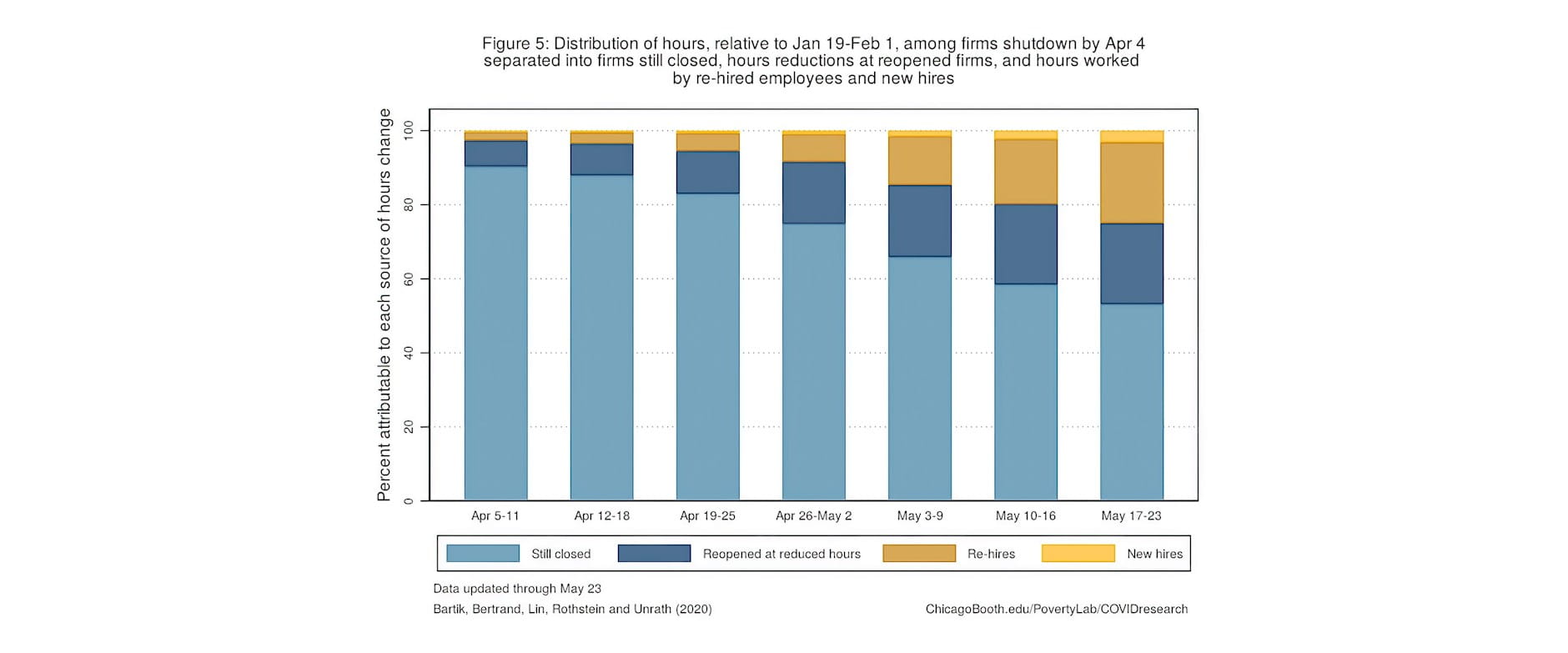

Figure 5 shows how hours have been restored (or are still missing) among firms that shut down before April 4. Across these firms, just over half of their collective baseline hours remain missing due simply to ongoing firm closures. Another 22 percent of hours are lost because reopened firms are operating at reduced scale. Counting all of the firms that have ever shut down, only about 25 percent of pre-shutdown hours have been restored. And again, almost 90 percent of those hours are worked by individuals employed by the business before it shut down.

DESCRIBING HOMEBASE FIRM CHARACTERISTICS

Our analysis is based on firms that use Homebase, which are not representative along many dimensions. They tend to be smaller than average, and concentrated in particular industries (such as food and drink and retail).

Below, we provide information on three characteristics of the firms in the Homebase data: the regions they are located in, the industries they operate in, and the number of employees they have. This information is based on firm characteristics between January 19 and February 1 and includes all firms operating during this time period, regardless of whether they have continued to operate through the COVID-19 crisis or not.

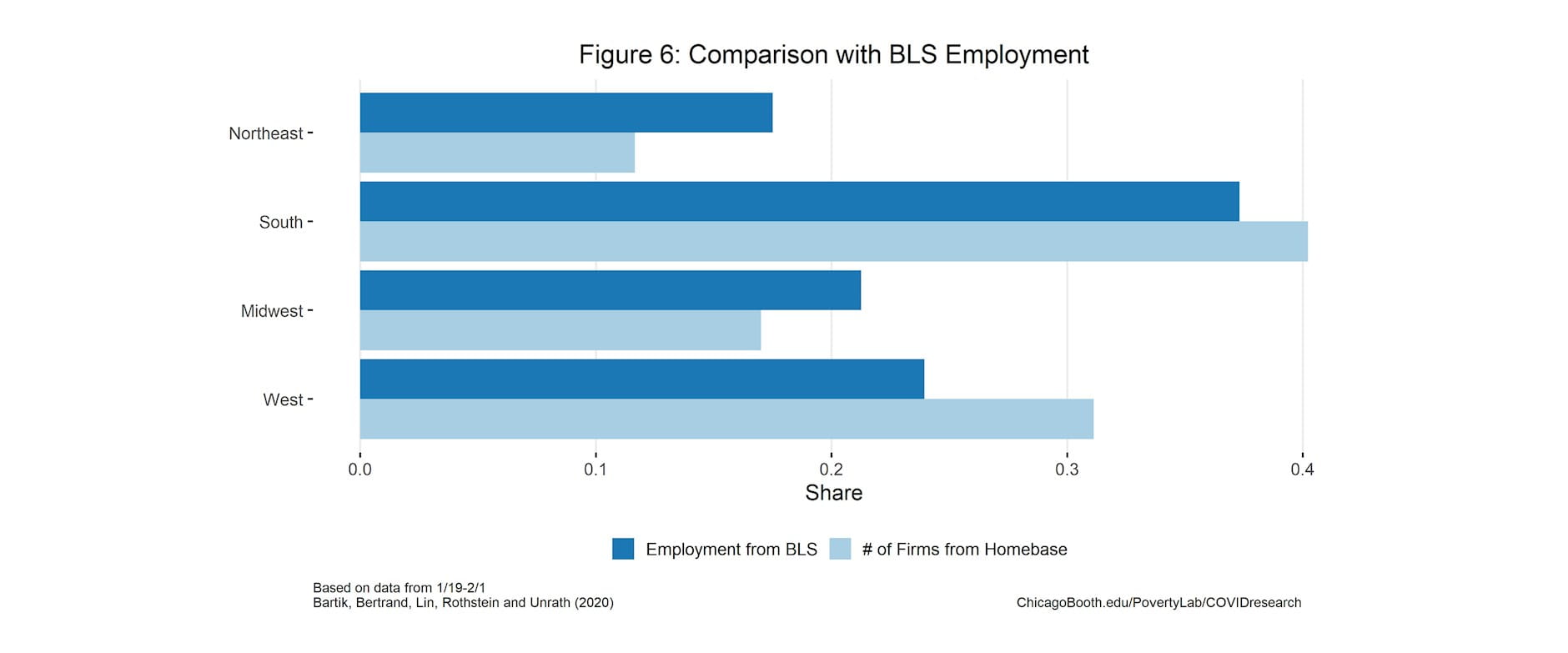

FIGURE 6: HOMEBASE FIRMS BROADLY MATCH THE DISTRIBUTION OF EMPLOYMENT ACROSS US REGIONS

This figure shows the share of Homebase firms located in each Census region (in light blue) and compares these shares to each region's share of total employment (in dark blue), as measured by the Bureau of Labor Statistics (BLS) data. Homebase firms are somewhat concentrated in the West region and less concentrated in the Northeast and Midwest than overall employment.

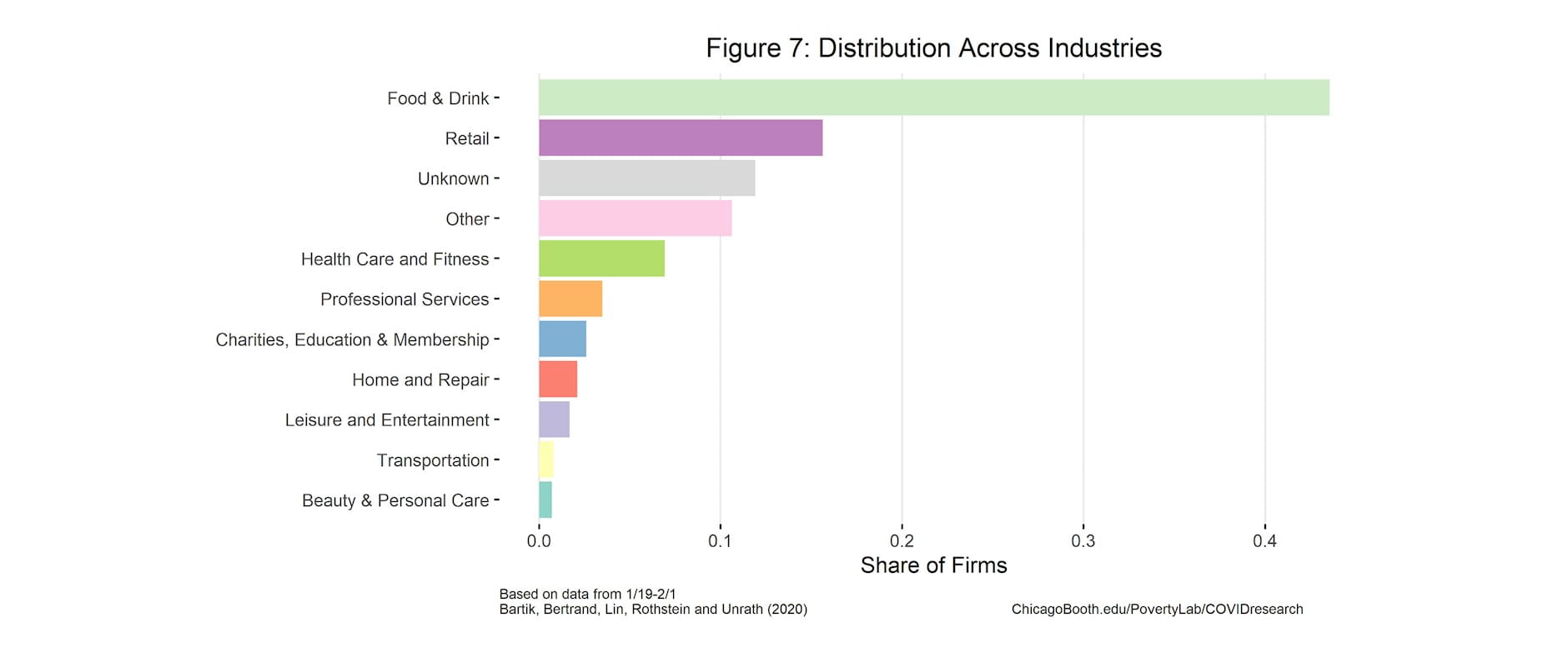

FIGURE 7: A MAJORITY OF HOMEBASE FIRMS ARE IN THE FOOD AND DRINK OR RETAIL INDUSTRIES

This figure shows the share of Homebase firms in each of the nine industry categories that Homebase uses. As might be expected given that Homebase offers scheduling and time-card software, Homebase firms are predominantly in industries like food & drink and retail that employ many hourly workers.

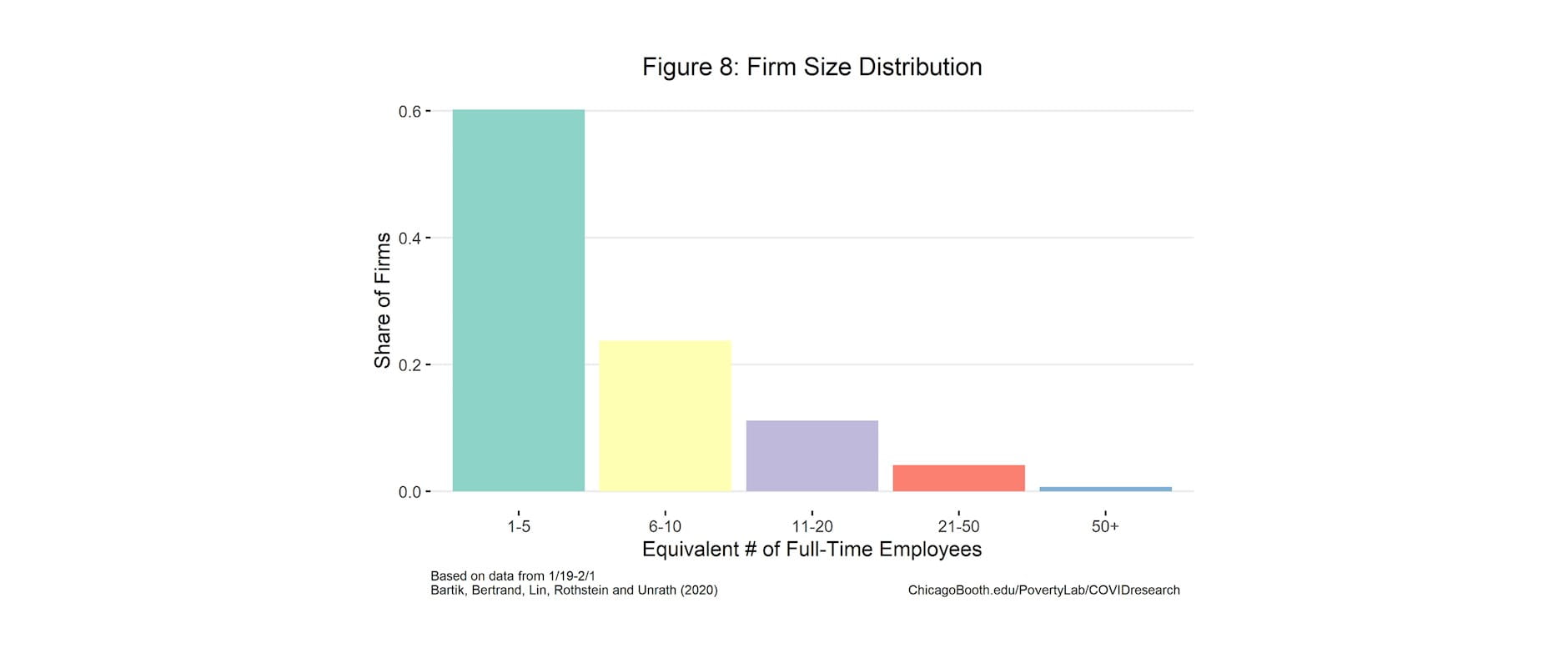

FIGURE 8: ALMOST ALL HOMEBASE FIRMS HAVE 50 FULL-TIME EQUIVALENT EMPLOYEES OR LESS

This figure shows the share of Homebase firms in each of five size categories. We define categories based on the number of hours worked at the firm between January 19 and February 1st, which we convert to full-time equivalent (FTE) workers by dividing by 40 hours per week. Roughly 60 percent of Homebase firms have one to five FTE employees (i.e., less than 400 hours worked in our two base period) and the vast majority have fifty or fewer FTE employees.

METHODOLOGY

Our analyses are based on data on hours worked at the establishment-worker-day level generously made available by Homebase. These data extend from January 1, 2020 through May 23, 2020. We aggregate the Homebase data to the firm-MSA-industry-day level.We restrict the sample to firms whose employees worked at least 80 hours between January 19 and February 1 and to states for which we observe at least 50 such firms. We refer to this two-week window as the “base period.” All analyses weight firms by their total hours during the base period.

In our analyses of weekly outcomes, we normalize each firm’s hours by dividing by the average hours worked per week over the base period at the firm. In our analyses of daily outcomes, we normalize by dividing by the average value of the outcome at the given firm on the same day of the week during our base period.For example, if total hours for a firm on Friday, March 13 was 100 and total hours for the same firm on Friday, January 24 and Friday, January 31 was 300, (150 on each day), the outcome variable total hours’ value would be .66. (This is 100 divided by (300/2), the average Friday hours in the base period.)

We use the data compiled by The New York Times on the timing of stay-at-home and shelter-in-place orders in different states.

Check back to Rustandy's Coronavirus Social Impact Research page for the latest results. Read the press announcement.

Authors

Alexander W. Bartik, Assistant Professor Economics, University of Illinois at Urbana-Champaign, and Research Affiliate, UChicago’s Poverty Lab; Marianne Bertrand, Chris P. Dialynas Distinguished Service Professor of Economics, University of Chicago Booth School of Business, and Faculty Director, Chicago Booth's Rustandy Center for Social Sector Innovation and UChicago’s Poverty Lab; Feng Lin, Research Professional, Chicago Booth; Jesse Rothstein, Professor of Public Policy and Economics, University of California, Berkeley, and Director, Institute for Research on Labor and Employment (IRLE) and California Policy Lab; and Matt Unrath, PhD Candidate, Goldman School of Public Policy, UC Berkeley, and Research Fellow, California Policy Lab

Acknowledgements

We thank Homebase and Ray Sandza in particular for generously allowing access to their data and sharing their time to answer questions and help us understand the data. We also thank Jingwei Maggie Li, Salma Nassar, and Greg Saldutte at Booth's Rustandy Center for Social Sector Innovation and Manal Saleh at the Poverty Lab for excellent assistance on this project and Michael Stepner for comments.

![]()

![]()

![]()