What scares investors? Not knowing the government’s next move.

- By

- September 11, 2014

- CBR - Economics

In July 2012, at a tense point in the eurozone debt crisis, European Central Bank Chief Mario Draghi had a moment that Bloomberg Businessweek later recalled as “superhuman,” and the Financial Times compared to Julius Caesar’s veni, vidi, vici. In a speech to investors in London, Draghi said the bank would do “whatever it takes” to preserve the euro—adding, “And believe me, it will be enough”—despite credit downgrades across the continent and seemingly imminent financial disasters in Greece, Portugal, and Ireland. The main thing Draghi was actually empowered to do was to print euros to buy the government bonds of struggling countries, and the market wanted to hear him say that he would.

Immediately after Draghi’s statement, financial markets across the world surged. “Those few words basically pulverized the eurozone debt crisis,” recalls Lubos Pastor, Charles P. McQuaid Professor of Finance at Chicago Booth. “Essentially, over the past two years, things have been getting better. Despite the lack of structural reforms, these words had a huge, huge impact.”

Draghi clearly had authority at the time of his statement. He was, after all, president of the “world’s second-most important central bank,” as the Economist put it, and he went on to announce a never-used bond-buying program later that year. But the power of his words was boosted by something else: policy uncertainty.

Before Draghi’s declaration, no one knew how far the ECB and eurozone governments were prepared to go to avoid financial disaster, or what effect their decisions would have. The not-knowing gave investors and businesses the jitters, thereby depressing the economy. Draghi’s “whatever it takes” largely allayed these concerns.

The Draghi example underscores recent thinking about policy uncertainty, whether it comes in the form of political bickering and inaction, or in other forms of government gridlock and stalemates. A growing body of research suggests that uncertainty has negative, measurable effects. Huseyin Gulen and Mihai Ion of Purdue University estimate that about two-thirds of the 32% plunge in corporate investments during the 2007–10 crisis period was attributable to policy-related uncertainty. The Peterson Institute for International Economics estimates that heightened fiscal-policy uncertainty saps real US GDP of about one percentage point—a loss of $150 billion each year.

As uncertainty can wreak havoc or be warded off with a few choice words, Draghi was either lucky or on the cutting edge of academic thinking. Now researchers and others interested in the topic are exploring what uncertainty is and how to use it, whether to make policy or profits.

Uncertainty is confounding by its very definition. In the economy, uncertainty can arise from a number of different corners, including wars, natural disasters, and, of course, government decisions—or indecision.

According to Steven J. Davis, William H. Abbott Professor of International Business and Economics at Chicago Booth, government-related policy uncertainty has three aspects that affect the decisions of people who collectively impact the economy. Tomas Hellebrandt, a senior researcher at the Peterson Institute for International Economics, notes that uncertainty may lead industries and firms to wait to invest, hire, or act. Households interpret political brinkmanship (the kind they saw during the US Congress’s 2013 debt-ceiling negotiations) as a threat to their financial well-being, and therefore buy and invest less, slowing the economy as they save their money and wait for better, safer times.

The suggestion that government can dampen the economy is controversial, in part because it has been politicized. Mitt Romney in August 2012 made policy uncertainty part of his campaign manifesto, citing work by Davis and coauthors saying that policy uncertainty reduced US gross domestic product by 1.4% in 2011, and that “restoring pre-crisis levels of uncertainty would add 2.3 million jobs in 18 months.” Then Princeton’s Paul Krugman, a self-proclaimed liberal, in an August 2013 column in the New York Times, attacked Romney’s thesis and Davis’s underlying research. “No, ‘economic policy uncertainty’—created, it goes without saying, by That Man in the White House—isn’t holding back the recovery,” he wrote, in a column titled “Phony Fear Factor.” “The truth is that we understand perfectly well why recovery has been slow, and confidence has nothing to do with it.”

John H. Cochrane, AQR Capital Management Distinguished Service Professor of Finance at Chicago Booth, says the debate should not be about whether or not policy uncertainty affects the economy, but to what extent it does so relative to other factors. “The question is, how much uncertainty is there? To what extent and by what mechanism does uncertainty influence GDP, investments, and stock prices? The answer is certainly more than zero and less than infinity,” Cochrane notes. “As economists, we need to look quantitatively at different potential causes of stagnation. There is an uncertainty effect, but how big is it in the face of all the well-known things that are dragging down the US economy?”

In 1952, Harry Markowitz, then a University of Chicago doctoral candidate, published an article in the Journal of Finance in which he showed how to construct a portfolio of financial assets to maximize expected returns for any given level of risk. Markowitz’s thinking, which eventually came to be known more commonly as “don’t put all your eggs in one basket,” helped earn him the Nobel Memorial Prize in Economic Sciences in 1990.

The study of risk, which in many research situations can be used interchangeably with uncertainty, became a defining feature of finance, something that set it apart from the study of economics. Future Federal Reserve Chairman Ben Bernanke, when still a professor at Stanford, wrote a well-received, 1983 paper on “Irreversibility, Uncertainty, and Cyclical Investment.” In it, he argued that when uncertainty is present—he didn’t specify the kind of uncertainty— investors will wait for more certainty before deciding whether to invest.

The University of California, Berkeley’s Christina Romer, chair of the Council of Economic Advisers from 2009 to 2010, used Bernanke’s earlier analysis about uncertainty plus consumer-spending data to draw conclusions about the economic turmoil of the 1930s in her oft-cited 1990 paper, “The Great Crash and the Onset of the Great Depression.” She argued that the collapse of stock prices in October 1929 was linked to a subsequent decline in output, as it caused consumers to become nervous and delay making large purchases.

Economic forecasters of the period, she pointed out, expressed doubts about the direction of the economy. Those doubts affected consumer behavior: consumer spending on durable goods such as home appliances and cars dropped precipitously in late 1929, while spending on perishable goods such as food actually rose slightly.

By the time Bernanke and Romer were up for confirmation for their respective positions, Congress and financial circles considered uncertainty an important enough concept that they discussed these papers as part of the confirmation hearings.

But uncertainty was not central to mainstream macroeconomic models, including those that guided the conduct of monetary policy. And only a few outlier economists in this area were looking at various measures of economic volatility, including stock-market volatility. Stanford University’s Nicholas Bloom, who describes a common view of business-cycle research in the mid-2000s after 20 years of economic calm as a “dusty downtown bar with a handful of old-timers,” attempted to quantify Bernanke’s assertion that rising uncertainty can cause investors and the economy to pause. Using stock-market volatility as a proxy for uncertainty, he noted a “panic spike” in uncertainty in the markets after large events, including the September 11, 2001, attacks on the World Trade Center and the Pentagon.

Bloom’s findings became all the more relevant with the 2007–10 financial crisis and the ensuing global downturn. He argued that if an individual firm makes decisions based on uncertainty, for example if it holds off on an investing decision because of a potential war in Ukraine, other firms are likely doing the same. And if you aggregate all of those decisions, uncertainty can be a catalyst of systemic risk. His data suggested that uncertainty shocks between 1962 and 2008 triggered immediate falls in national output and unemployment, followed by rapid rebounds once the uncertainty was resolved.

Bloom’s findings about the impact of collective uncertainty coincided with a change in government activity. US President Barack Obama took office in January 2009 with an ambitious policy agenda, including overhauling the health-care system. The Federal Reserve had given up adjusting interest rates to boost the economy and had begun purchasing billions of dollars’ worth of government and mortgage bonds each month.

“In the wake of the financial crisis and the Great Recession, we were living through a period with a great deal of uncertainty about what policy actions would be undertaken and what their effects would be,” says Davis. “There was a sense that we stood at an unusual juncture with a great deal of uncertainty about policy actions and their consequences.”

Government seemed to be a source of widespread uncertainty. In January 2010, Davis—with Nobel laureate Gary S. Becker, who passed away this year, and Kevin M. Murphy, George J. Stigler Distinguished Service Professor of Economics at Chicago Booth—wrote an op-ed in the Wall Street Journal arguing that the economy had been hampered by uncertainty stemming from governmental proposals, including one to increase marginal tax rates for higher-income earners, one to change tax rates for greenhouse gas–producing facilities, and one to rework antitrust policy.

That year Bloom and Davis teamed up with Scott R. Baker, then a doctoral candidate at Stanford and now a professor at Northwestern University’s Kellogg School of Management, to measure whether that was the case. They performed computer-automated searches on the digital archives of 10 large American newspapers, including USA Today, the Chicago Tribune, the New York Times, and the Wall Street Journal, to determine the frequency of articles about policy-related economic uncertainty. To evaluate and refine the computer-automated method for identifying articles about economic-policy uncertainty, they worked with a large team of research assistants to review and hand-code several thousand randomly sampled newspaper articles.

Figuring that the articles could be a proxy for businesspeople’s and households’ concerns about policy-related uncertainty, they used their counts to create the Economic Policy Uncertainty Index (EPU), which indicates the level of policy uncertainty in given periods.

To check their proof of concept, they used the same methodology to create an index measuring uncertainty about stock-market returns, rather than economic policy. And they compared their index to a widely used market measurement of stock-market uncertainty: the Chicago Board Options Exchange Market Volatility Index (VIX), sometimes known as the “fear index.” Their newspaper-based index and the VIX were highly correlated, which led the researchers to believe that their methodology worked, at least in principle.

They also compared their newspaper measure with the Beige Book, a review of economic activity in the 12 Federal Reserve districts, which the Federal Open Market Committee publishes every six weeks. Again, “the two sources told us broadly similar stories,” says Davis.

Now the researchers provide historical, daily, and monthly US policy-uncertainty indexes. They administer a debt-ceiling index, which measures uncertainty relating to US debt-ceiling issues and potential federal shutdowns.

They also have indexes measuring policy uncertainty in Europe, China, Canada, India, and most recently Russia.

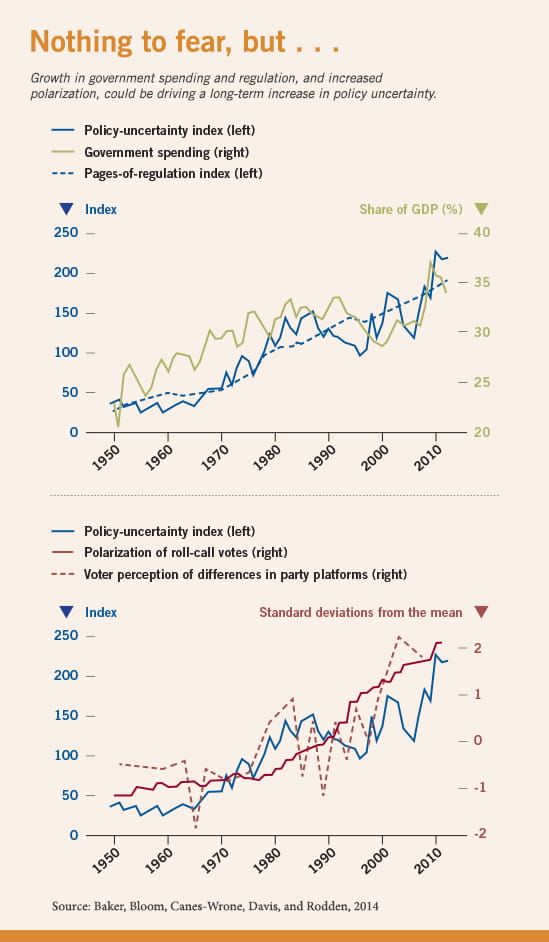

The indexes indicate that policy uncertainty grew significantly worldwide after 2007—and hit a high in the US in August 2011 when members of Congress fought over whether or not to raise the amount of money the government can borrow. According to the data, uncertainty in the US from 2008 to 2012 was double what it averaged in the previous 25 years, a span that included such traumas as the 1987 stock-market crash, the disputed 2000 presidential election, and 9/11. It has spiked several times since the 1960s, often during closely contested presidential elections, and in cases of political brinkmanship.

The researchers attribute the increasing uncertainty in part to the way the government is taking in and spending money. In the early 1950s, government spending was about 20% of GDP; it was 35% of GDP by 2010. Moreover the rules governing taxing and spending has grown more complex. Since 1960, the Code of Federal Regulation, an annual publication that compiles all federal regulations, has grown more than sixfold.

They suggest that the rise in political polarization is also causing increased uncertainty. In the US, presidential elections have been hotly contested, party leaderships have diverged sharply, and partisan control of Congress has changed frequently. “Investors in the US economy traditionally take solace in the extensive checks and balances embedded in the American constitution,” the researchers write, adding that divided government, Senate obstructionism, and even opposition within political parties often derail presidential policy initiatives.

“In recent years, however, these sources of status quo bias often reinforced rather than reduced policy uncertainty.”

Krugman, in the New York Times, argues the methodology used to create the primary index, the US EPU, is flawed. “It relied in part on press mentions of ‘economic policy uncertainty,’ which meant that the index automatically surged once that phrase became a Republican talking point,” Krugman writes. Davis, in a December 2013 response, counters that the newspaper methodology has been verified by three other components, all of which showed elevated levels of policy uncertainty from 2009 to 2012.

Krugman also argues that, as the index dropped in 2013 and the economy did not take off, policy uncertainty didn’t cause the slowdown. Rather, the slowdown caused uncertainty. But “that argument fails to persuade because many factors affect economic performance,” Davis writes. Citing tax hikes, restraints on federal spending, and tight local budgets, among other factors, he argues that slow US growth in 2013 doesn’t refute the claim that policy uncertainty matters. Moreover, he writes that even if the recession caused policy uncertainty, that “doesn’t mean it doesn’t play a role in the economy, and it doesn’t mean we don’t need to measure it.”

Several of Davis’s colleagues believe that government-related uncertainty is a factor whose effects can be seen in financial markets. After Pastor and Pietro Veronesi, Roman Family Professor of Finance at Chicago Booth, noticed that news about government actions moved markets during the 2007–10 financial crisis, they created a model to describe what was happening.

Their model suggests that in most Western-style governments, where a government usually acts in investors’ best interests, unexpected government policies can spook the market. As investors expect their government to make good policy decisions, such decisions will send the market up a little or not at all when the government acts as expected. But if the government makes a bad decision, such bad news will be unexpected, and markets will drop punishingly as

a result.

The research also suggests that politicians can move markets. Even if a politician has little new to say, investors search for signals about what action he or she might take in the future. And if a politician says something important, markets often respond strongly. Veronesi points to Greece, and in particular to the moment the European Union agreed on the bailout package for the country in October 2011. Stock markets responded enthusiastically, with French and German stocks rising by more than 5% in one day. But on November 1, 2011, Greek Prime Minister George Papandreou called for a referendum.

“That’s the only thing he did, he just called for a referendum,” Veronesi says, “and prices went back down”—because investors believed the referendum might precipitate a Greek exit from the eurozone.”

Moreover the strength of the economy affects the amount investors will care. “When economic conditions are strong, politicians talk and talk, but markets really don’t pay much attention,” says Pastor.

After all, a politician who presides over a strong economy isn’t likely to reinvent policies. But in a crisis, as investors know, politicians feel compelled to do something.

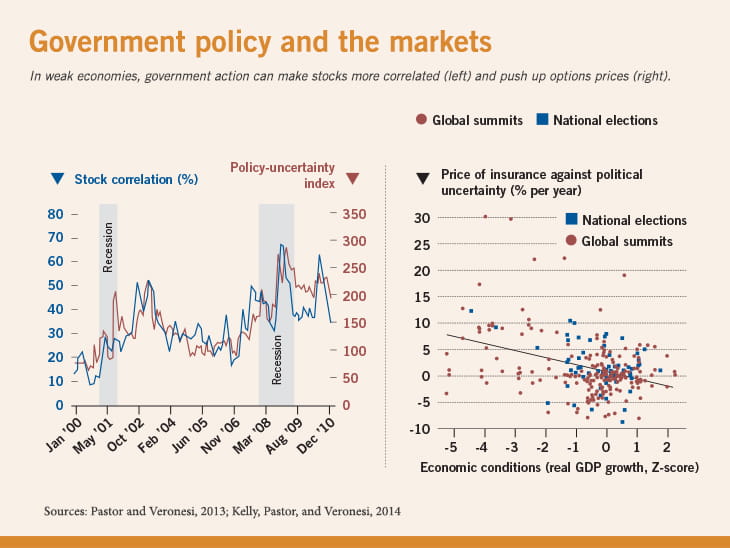

The researchers verify their theoretical findings using data from the EPU and the stock-options market. Working with Bryan T. Kelly, associate professor of finance and Richard N. Rosett Faculty Fellow at Chicago Booth, they compare options prices around the time of global summits or elections. In doing this, they isolate and focus on uncertainty about what a government, or group of governments, is going to do, not on the impact of the eventual action.

They see that prices are more volatile and correlated when uncertainty levels are high. But also, the researchers get a glimpse of how much uncertainty is costing investors, as options data allow them to see how much investors and businesses are paying to insure themselves against several risks associated with uncertainty surrounding the event.

Events that are more uncertain have bigger impacts on asset prices. It costs 5% more to buy insurance against stock-market fluctuations when an election is approaching, for example. Moreover the data verify that the strength of the economy affects the amount investors will pay to insure against risk. When the economy is weak, the same insurance costs 8% more than it does in stable times, when no election is imminent. When the economy is strong, the insurance costs just 1% more.

And when an uncertain situation is resolved, investors celebrate. In separate research, Dacheng Xiu, assistant professor of econometrics and statistics at Chicago Booth, working with Dante Amengual of CEMFI in Spain, finds that short-term market volatility declines when uncertainty is resolved, just as it does when good news—such as a rise in employment figures—is released. For example, when the EU and the International Monetary Fund made an unprecedented loan package to rein in its sovereign-debt crisis in May 2010, the (US) VIX dropped 36%, while the VStoxx Index (a similar volatility gauge specifically tailored to the European equity markets) had the biggest drop in its eleven-year history, and worldwide equity markets shot up.

“Behind the resolution lay an enormous political contest and a vast uncertainty about the future of the European Union, its currency, and its economy. While the market calmed down momentarily, the impact of this bailout on long-term uncertainty was open to question,” Xiu says. “We devise a model that can be used to quantify the short-term and long-term impact of policy resolutions on uncertainty.”

And when it comes to the US market, “It turns out most volatility drops during crises are related to the Federal Reserve chairman’s speeches and to FOMC statements,” he says. Even though the Federal Reserve often soothes the market in hard times, Xiu and Amengual caution investors, particularly volatility sellers, not to ignore tail risk, as the size and scope of the intervention is uncertain.

As the concept of policy uncertainty is refined, some researchers are identifying specific sources of policy uncertainty, such as trade policy. But a big source of uncertainty lies with central bankers such as Draghi.

The US Federal Reserve Bank, the Bank of England, the Bank of Japan, and the European Central Bank have a huge impact on the markets and economy, and investors carefully parse statements from central bankers to divine their meaning. However, even when these bankers try to speak and act clearly—as Ben Bernanke and Janet Yellen have tried to do—their messages can fuel uncertainty, find Drew D. Creal, associate professor of econometrics and statistics at Chicago Booth, and Jing Cynthia Wu, assistant professor of econometrics and statistics at Chicago Booth.

Wu says that what matters is what bankers say and how they say it. For example, at the Federal Reserve, “for some periods, they will tell you exactly how long the zero lower bound will stay,” Wu says, referring to the state of the federal funds rate when it is near zero. Other times the Fed will offer contingencies, depending on the unemployment rate or inflation, and those contingencies create uncertainty. How investors interpret what the Fed says is also important. “Even though the Federal Reserve can convey that they will keep interest rates low for another year or so, whether the market believes that as fact is another question,” says Wu.

Creal and Wu use short- and long-term interest-rate volatility to measure uncertainty. They calculate that monetary-policy uncertainty rose only until the end of the Great Recession, in 2009, and has been low since then.

The data also suggest that short- and long-term uncertainty can cause unemployment rates to rise but have opposite effects on inflation. After short-term uncertainty increases, inflation decreases. But a rise in long-term uncertainty is generally followed by rising inflation.

The overall impact of uncertainty on inflation can change depending on the period. Right before the Great Recession, both types of uncertainty spiked, but ultimately inflation fell, as short-term uncertainty exhibited strong downward pressure. But during the Great Inflation of the 1970s, short- and long-term uncertainty also rose. But long-term uncertainty had the stronger impact, and inflation increased.

To be sure, certainty is not necessarily a cure for economic ills. “A lot of businesses are not investing, and it isn’t because they are unclear on what is going to happen. They have a pretty good idea about what the government will do, and they don’t want to invest their funds because they don’t see any way to make a profit in the current regulatory and tax environment,” Cochrane says.

But uncertainty may be an economic damper. The IMF is using the EPU to describe the state of the economy and concerns facing it, and as an input into statistical models of national economic performance. Bond giant Blackrock has created its own policy-uncertainty indexes to measure the impact of policy uncertainty on investors.

The MacArthur Foundation in 2013 awarded a $250,000 grant to the Becker-Friedman Institute for Research in Economics—a collaboration of Chicago Booth, the University of Chicago’s department of economics, its law school, and the Harris School of Public Policy—to bring the academic findings on policy uncertainty to the attention of policymakers. The institute is creating a series of brief videos for lawmakers, nongovernmental organizations, policy institutes, and think tanks. The hope is that policymakers could use the findings to reduce, or at least avoid aggravating, policy uncertainty.

“For society, it’s good to know there’s a cost to political bickering,” Pastor says. “If you engage in political brinkmanship . . . there’s a big cost attached to that. And hopefully these calculations will help deter similar actions in the future.”

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.