How Eugene F. Fama Has Left His Mark on Industrial Organization

The Nobel laureate is best known for work on efficient markets. But he also helped develop event studies, which have been used extensively in the field.

- By

- May 10, 2017

- CBR - Economics

With the exception of his well-known work on the theory of the firm, Chicago Booth’s Eugene F. Fama is not mentioned as much as he should be in the industrial-organization literature. The reason is that one of the techniques that Gene was instrumental in developing, the event study, is used so routinely without attribution in industrial organization that I suspect many economists in the field are unaware that he helped figure it out. If Gene were a young assistant professor awaiting a tenure decision, or egotistical about the number of citations his work receives, I am sure he would be greatly upset. However, that is not a description of Gene.

In this brief space, I cannot comprehensively review all the topics in industrial organization influenced by event studies, but let me hit just a few key ones, with apologies to the many authors whom I do not have space to mention. I’ll end with a brief discussion of another area where Gene’s work is likely to influence industrial organization: the risk characteristics of small-value firms.

Merger policy is a fundamental topic in industrial organization. It is of practical as well as academic interest, as staffs of PhD economists at the Federal Trade Commission and the Department of Justice routinely have to figure out which mergers to allow and which to challenge.

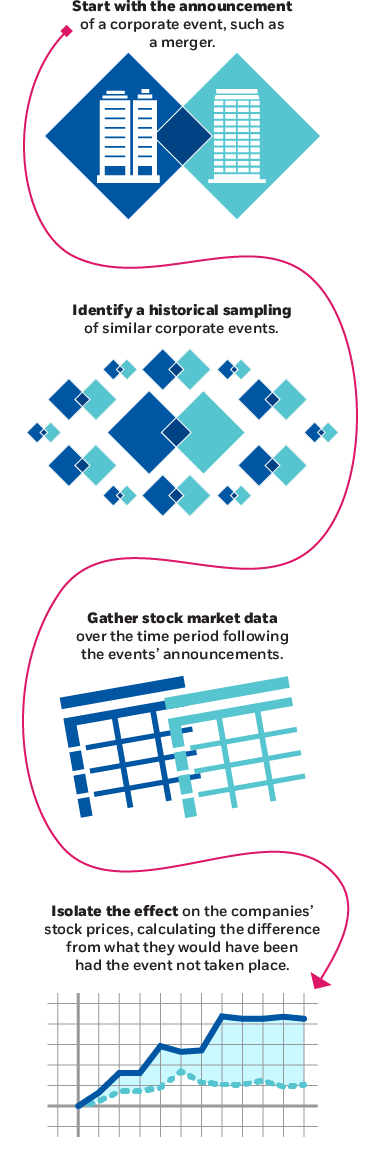

Event studies clarify impact of corporate moves

Chicago Booth's Eugene Fama helped figure out the event study, a tool economists use to assess an individual corporate event's effect on the company's market value.

The recent Antitrust Modernization Commission was charged with analyzing whether merger policy in the United States should be changed. Event-study literature about mergers was one of the key areas of academic research it examined.

Starting in 1983 with Dartmouth’s B. Espen Eckbo and Robert Stillman, now of Charles River Associates, industrial-organization economists have asked how the anticompetitive features of a merger could be analyzed by event studies. The logic goes as follows: suppose Firm A announces that it will merge with Firm B, and the value of the sum of the two firms postannouncement exceeds the sum of the values of the two firms before the announcement. That increase could occur either because the merger is efficient or because the merger will reduce competition and lead to elevated pricing. If the merger is expected to lead to higher prices, the rivals of the merged firm will benefit. However, if the merger will not increase market power but instead will create a more efficient firm, the values of the rivals of the merged firm should fall. So, by examining the response of rival firms’ stock prices to a merger announcement, regulators can tell whether the proposed merger represents increased efficiency or increased monopoly. This procedure exploits the more general and deeper shift in understanding introduced by Gene’s efficient-markets hypothesis, that stock prices collect, reflect, and convey information otherwise held by dispersed market participants.

There are, of course, many caveats to such an analysis. For example, an event study requires that one define when the information about the merger starts leaking out to the market, how expectations change along the lengthy antitrust review process, and whether one can look at only equity values and not debt. Moreover, because firms sell many different products, the value of the firm may consist of so many industry segments that the effect of a merger in one segment will be hard to detect by examining the effect on the firm’s value.

Despite all these caveats, the results of these studies have been remarkably consistent over time. Mergers don’t seem to create market power but do seem to create efficiencies. There is an overall gain in value to the merged firm somewhere in the range of 0–10 percent above the value of the separate firms’ values, and that gain seems unrelated to market power. This result, of course, does not mean that mergers never create market power—just that any attempt by merger authorities to become more stringent in merger enforcement must recognize that, given our limited ability to identify such anticompetitive mergers ex ante, any significant toughening of standards runs the risk of deterring efficiency-enhancing mergers.

There may be anticompetitive mergers going on, but government agencies don’t seem to be able to identify them in their challenges.

Event studies can also give guidance on whether government challenges to mergers have been perceived by the market as preventing antitrust harm. If the government challenges a merger that would lead to higher consumer prices because of the elimination of competition, that challenge should lead to a decline in the value of the merged firm’s rivals, who would benefit from the general increased price level. In a 2004 research paper, Tulane’s C. Edward Fee and University of Pittsburgh’s Shawn Thomas investigate that possibility and do not find evidence to support it. There may be anticompetitive mergers going on, but government agencies don’t seem to be able to identify them in their challenges.

More research is needed to reconcile these event studies with postmerger pricing and accounting information. If the merged firm is more efficient than the premerger firms, presumably measured profits should rise. That link has been hard to establish. Perhaps this is because of the difficulty of using accounting information, though I find that explanation unsatisfying. Some detailed studies of individual mergers have been more successful. There is evidence that CEOs who fail to deliver the anticipated value of a merger get replaced. But there is more work to be done to reconcile these results with the stock-price behavior documented by event studies. Moreover, there have been relatively few merger retrospectives on pricing in the industrial-organization literature, but that is changing. Linking up these postmerger studies on profits and individual pricing with event studies at the time of the merger would fill a gap in the literature. All of these advances are made possible by Gene’s contribution from decades before.

The effect of regulation is another question of great interest to industrial-organization economists. University of Rochester’s G. William Schwert describes clearly how event studies can assist in the study of regulation. Since that article was published in 1981, a large number of studies have done what Schwert suggests. Event studies have proven enormously valuable here, though again there are many complicated issues related to identifying the right event windows and figuring out how the regulations have affected the riskiness of the firms. The obvious question is how proposed and implemented regulations have affected the value of firms in the industry. If regulation protects consumers by limiting the exercise of market power on prices, regulations should reduce the profits of firms and lower their value. On the other hand, if producer groups use regulations to their advantage, for example by reducing competition, greater regulation might increase stock market value.

There have now been numerous event-study investigations of the effects of regulation and deregulation. The Federal Reserve’s Robin A. Prager used an event study to show that the creation of the Interstate Commerce Commission (ICC) in 1887 can be viewed as an attempt by the railroads to create a regulatory authority that would limit the amount of railroad competition, to the detriment of consumers. The creation of that regulatory authority is associated with an increase in the value of railroads. Early court decisions that limited the power of the ICC to protect railroads from competition typically reduced the value of railroads. The ICC subsequently was captured by the customers of railroads and wound up harming the value of railroads.

There also have been numerous studies of the effect of deregulation of various industries using event studies. For example, MIT’s Nancy L. Rose uses an event study to show that deregulation of trucking in the 1980s led to large declines in the value of certain trucking firms, suggesting that the earlier regulations were used to prevent competition in trucking. University of Oregon’s Larry Y. Dann and University of Florida’s Christopher M. James find that the permission to issue variable-rate money-market certificates in the 1970s lowered the value of savings and loans. The 1980 deregulations, which allowed banks to offer a greater variety of services, helped large banks and hurt small ones. Central Connecticut State University’s Kathy Czyrnik and University of Connecticut’s Linda Schmid Klein use event studies to show that repeal of the Glass-Steagall Act increased the value of commercial and investment banks.

Recent literature has shown that it is not small firms, but rather young ones, that have growth prospects distinguishing them from other firms.

Event studies have also proven useful in industrial organization to measure the value of reputation. Reputation is hard to evaluate; but by looking at what happens to stock prices when an event hurts a firm’s reputation, one can quantify the harm to reputation aside from the direct harm from the unfortunate event. For example, AQR’s Mark L. Mitchell and Clemson University’s Michael T. Maloney examined what happens to the value of an airline when it experiences a crash. They find that the crash has a negative effect on firm value only if the crash was due to pilot error. If it was not pilot error, then their interpretation is that the airline has insurance to cover the direct costs of the crash and there is no further reputational loss.

Event studies have also been useful in the current controversy regarding patent-assertion entities, sometimes pejoratively referred to as patent trolls. The concern is that some firms do nothing but amass a large portfolio of patents of questionable validity and then go around suing lots of other firms, which settle the case rather than fight it in court in order to avoid high litigation costs. Such suits could deter innovative activity and could be viewed as a tax on producing firms. Event studies have shown that such suits have decreased the value of defendants in lawsuits by about $500 billion over the last decade. There is much concern that the original inventors of these patents obtain little of this bonanza, so there are no positive incentive effects on invention.

I conclude with a topic not associated with event studies. The article by Fama and Dartmouth’s Kenneth R. French, “Common Risk Factors in the Returns on Stocks and Bonds,” focuses on small-value firms. There is literature in industrial organization that looks at the birth and death of small firms. (As far as I know, it does not identify value firms.) This literature recently has shown that it is not small firms, but rather young ones, that have growth prospects distinguishing them from other firms. Reconciling and further investigating the connection between this literature in industrial organization and the finance literature in this area should have big research payoffs in identifying the risks facing small firms, and potentially in understanding the source of the small-stock and value-stock premiums in asset markets, and resolving puzzles such as the surprisingly bad stock market performance of small-growth firms, identified by Fama and French. Another great contribution from Gene, seemingly unrelated to industrial organization, may yet prove its importance in that area.

Dennis W. Carlton is David McDaniel Keller Professor of Economics at Chicago Booth. This essay is excerpted from The Fama Portfolio, Selected Papers of Eugene F. Fama, edited by John H. Cochrane and Tobias J. Moskowitz, University of Chicago Press, copyright 2017.

- Gregor Andrade, Mark Mitchell, and Erik Stafford, “New Evidence and Perspectives on Mergers,” Journal of Economic Perspectives, Spring 2001.

- James Bessen, Jennifer Ford, and Michael J. Meuer, “The Private and Social Costs of Patent Trolls,” Regulation, Winter 2011–12.

- Kathy Czyrnik and Linda Schmid Klein, “Who Benefits from Deregulating the Separation of Banking Activities? Differential Effects on Commercial Bank, Investment Bank, and Thrift Stock Returns,” Financial Review, April 2004.

- Larry Y. Dann and Christopher M. James, “An Analysis of the Impact of Deposit Rate Ceilings on the Market Values of Thrift Institutions,” Journal of Finance, December 1982.

- B. Espen Eckbo, “Horizontal Mergers, Collusion, and Stockholder Wealth,” Journal of Financial Economics, April 1983.

- Eugene F. Fama, Lawrence Fisher, Michael C. Jensen, and Richard Roll, “The Adjustment of Stock Prices to New Information,” International Economic Review, February 1969.

- Eugene F. Fama and Kenneth R. French, “Common Risk Factors in the Returns on Stocks and Bonds,” Journal of Financial Economics, February 1993.

- C. Edward Fee and Shawn Thomas, “Sources of Gains in Horizontal Mergers: Evidence from Customer, Supplier, and Rival Firms,” Journal of Financial Economics, December 2004.

- Teresa Fort, John Haltiwanger, Ron S. Jarmin, and Javier Miranda, “How Firms Respond to Business Cycles: The Role of Firm Age and Firm Size,” IMF Economic Review, August 2013.

- Gregg A. Jarrell and Sam Peltzman, “The Impact of Product Recalls on the Wealth of Sellers,” Journal of Political Economy, June 1985.

- Steve Kaplan, “Mergers and Acquisitions: A Financial Economics Perspective,” Testimony before the Antitrust Modernization Commission, February 2006.

- Marcia H. Millon-Cornett and Hassan Tehranian, “Stock Market Reactions to the Depository Institutions Deregulation and Monetary Control Act of 1980,” Journal of Banking and Finance, March 1989.

- Mark L. Mitchell and Michael T. Maloney, “Crisis in the Cockpit? The Role of Market Forces in Promoting Air Travel Safety,” Journal of Law and Economics, October 1989.

- Robin A. Prager, “Using Stock Price Data to Measure the Effects of Regulation: The Interstate Commerce Act and the Railroad Industry,” Rand Journal of Economics, February 1989.

- Nancy L. Rose, “The Incidence of Regulatory Rents in the Motor Carrier Industry,” Rand Journal of Economics, 1989.

- G. William Schwert, “Using Financial Data to Measure Effects of Regulation,” Journal of Law and Economics, April 1981.

- Robert Stillman, “Examining Antitrust Policy toward Horizontal Mergers,” Journal of Financial Economics, April 1983.

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.