In Commercial Real Estate, Less Risk ➔ More Reward

- By

- September 02, 2014

- CBR - Finance

When it comes to commercial real estate, US pension plans—and other large global investors—have traditionally invested conservatively. But mounting retiree claims and worries of underfunding are driving them into riskier ventures. US pension plans have chalked up this additional risk-taking as necessary for ensuring enough growth to fulfill retirement promises to millions of American workers.

They may want to rethink their approach. On average, pension funds would have produced better returns by sticking to their conservative instincts, according to research by Clinical Professor Joseph L. Pagliari Jr., with research assistance provided by former student and now Balyasny Colony Funds’ real estate analyst Camilo Varela. He wrote up his findings for the Pension Real Estate Association, but they apply to any investor, be they institutions or individuals, in commercial real-estate funds.

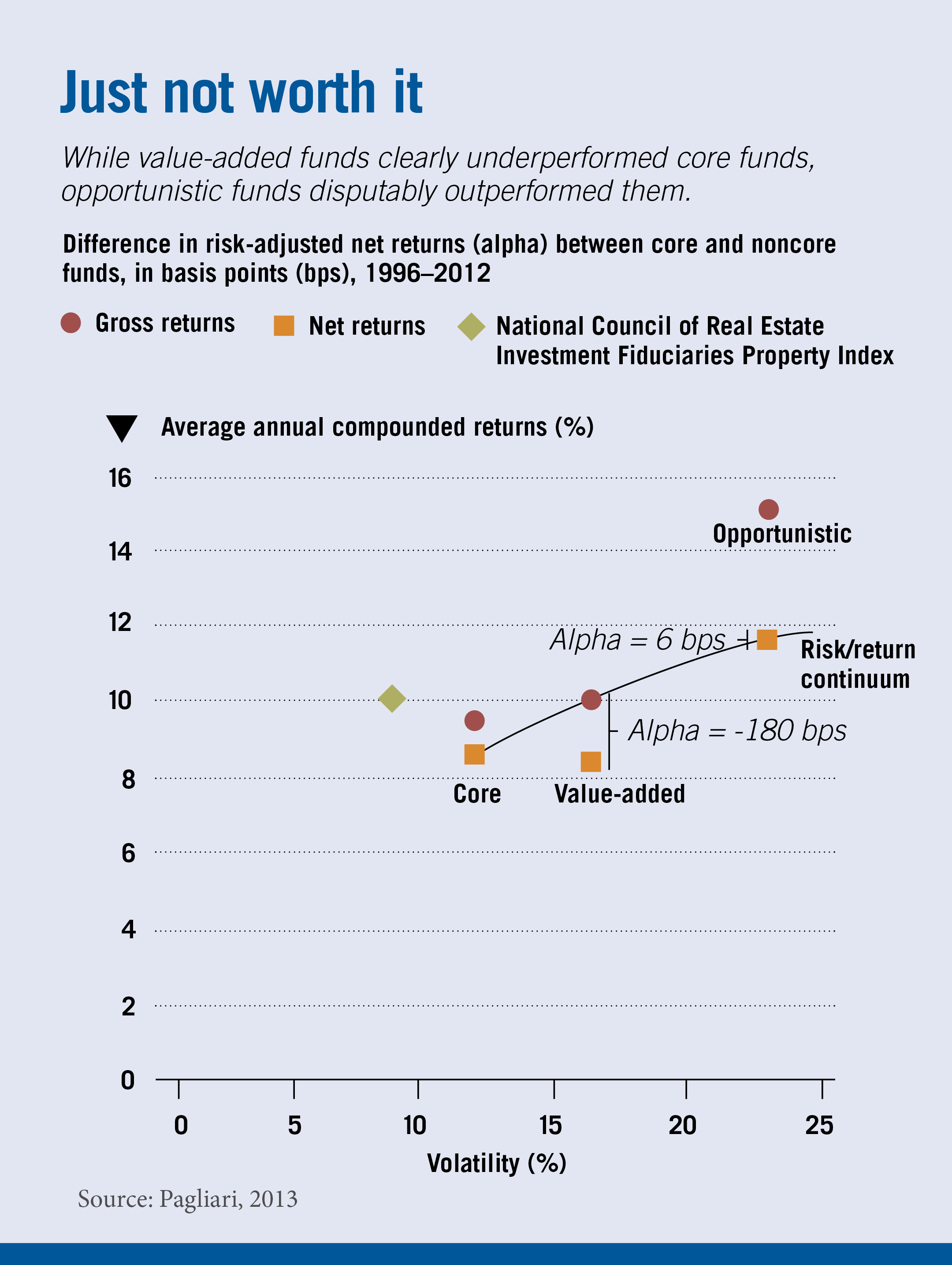

Consider the risk spectrum of commercial real estate: low risk is exemplified by core funds, medium risk by value-added funds, and high risk by opportunistic funds. Pension plans have traditionally invested in core funds, filled with stable properties such as fully rented apartment buildings and office complexes, financed with moderate leverage (of approximately 25%). To boost returns, many pension funds have increased their allocations to value-added funds and opportunistic funds, which hold a range of riskier properties, including new developments, distressed properties, and foreign projects, and are financed with more aggressive leverage ratios (of more than 50%).

Looking at 17 years of fund data, Pagliari finds that those riskier investments have not paid off. Consider the accompanying graph. Investors in an index of value-added funds had lower net returns than investors in core funds, after having adjusted for risk, by approximately 180 basis points per year. As for the even riskier opportunity funds, Pagliari suggests those may not, on average, be worth the danger to investors either. An index of opportunity funds had higher returns than investors in core funds, after having adjusted for risk, by approximately 6 basis points per year. This result occurred only after including the financial crisis of 2007–10—as before then, opportunity funds underperformed core funds on a risk-adjusted basis. The finding that opportunity funds outperformed less risky funds during the crisis, says Pagliari, confounds logic.

One reason for the underperformance is fees. As the riskiness (and, presumably, the expected return) of the fund increases, so too do the incentive fees paid to the general partner or fund manager. Core funds compete for investors on the basis of low fees and low risk. But managers of value-added and opportunity funds charge higher fees in much the same way that hedge funds charge investors more than mutual funds do. And as is often the case with hedge funds, the higher fees on the riskier funds can eliminate the advantages for investors of higher gross returns.

Pagliari illustrates this point with an analysis meant to help investors critically study and compare the net-return potential of funds with the popular “pref-and-promote” fee structures. In this arrangement, the manager takes a portion, or a “promote,” of all profits above a predetermined preferred rate of return, or a “pref.” Many institutional investors like this type of incentive fee structure because they believe it aligns the interests of the manager with the investor—a classical principal/agent problem, which occurs whenever one person, the agent, makes decisions on behalf of another person, the principal.

However, these pref-and-promote structures have a profound impact on the investor’s net return. Moreover, the reported volatility of net returns understates the true volatility of the investor’s return, because the promote claims a portion of the upside. Pagliari points out that the pref-and-promote structure does not limit the investor’s downside risk, as the manager’s incentive fee will be zero whenever the fund earns a gross return below the pref—even when the fund loses money.

Pagliari also argues that investors often don’t adequately account for what the promote is costing them, both in terms of the investor’s potential net return and the manager’s incentives. With regard to the former, he offers calculations to help investors better understand how the promote places a drag on the investor’s expected net return. With regard to the latter, he suggests lowering both the preferred return and the promoted interest as a way to compel fund managers to expend more effort and take more prudent risks.

Pagliari gives several reasons to be skeptical of the reported volatility of returns on riskier strategies. For example, widely reported indices indicate that, during the 2007–10 financial crisis, the volatility of the opportunity funds’ returns declined relative to the volatility of core funds. (All indices reported greater volatility during this time, but the volatility of opportunity funds’ returns increased less dramatically than that of the core funds.) This result seems implausible given that opportunity funds invest in riskier assets and employ more leverage than core funds do. Riskier assets suffer more severe devaluations in the “flight to quality” that accompanies any financial crisis, and leverage also contributes to greater volatility.

Problems with fund reporting make the riskier strategies appear more lucrative for investors than they really are. All funds have self-reported returns, but while core funds have strict rules for reporting updated appraisals and performance data, many of the higher-risk funds do not. During the financial crisis, about 13% of the opportunistic funds stopped reporting. Some of them presumably went out of business, whether through bankruptcy or some other form of complete liquidation, Pagliari says. This form of survivorship bias results in overstating reported average returns for these opportunistic strategies and understating their volatility. So Pagliari restated the returns for the index of opportunity funds, estimating what returns would have been had none, some, or all of the firms gone out of business. In a scenario where half of the missing funds had gone out of business, the average gross annual return on opportunity funds decreased by nearly two percentage points, to just over 15%, and it increased volatility about one-and-a-half percentage points, to 23%.

In order to make the risk-adjusted comparisons, the paper adds more leverage to core funds, which increases both average return and volatility. This application of the “law of one price”—an economic concept that says two or more things must sell for the same price regardless of where they are—creates a risk/return continuum that any institutional investor could have utilized.

Had investors invested in core real-estate funds using more leverage, between 40% and 60% rather than the 25% historically utilized, they would have produced net returns that on a risk-adjusted basis would have outperformed the value-added funds by 180 basis points per year. They would have also produced net, risk-adjusted returns that would have essentially matched the performance of the opportunity funds—without having raised troublesome valuation questions during the financial crisis.

As is, Pagliari’s research indicates that investors who buy into aggressive commercial-real-estate funds generally add more risk to their portfolios, not better returns.

Joseph L. Pagliari Jr., “An Overview of Fee Structures in Real Estate Funds and Their Implications for Investors,” Research report for the Pension Real Estate Association, 2013.

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.