Actively Managed, but More Index-Like

Infographic: Mutual-fund portfolios have become more liquid.

- May 15, 2018

- CBR - Finance

When investors consider the liquidity of a stock portfolio, they are usually interested in how readily the underlying holdings can be bought or sold. For example, a portfolio of large-cap equities, or heavily traded stocks of big companies, is generally considered to be more liquid than a portfolio of small-cap equities, or lightly traded stocks of small ones. Although the focus on the average liquidity of the portfolio’s holdings is largely correct, it paints an incomplete picture, according to research by Chicago Booth’s Lubos Pastor and University of Pennsylvania’s Robert F. Stambaugh and Lucian A. Taylor. The portfolio’s construction matters too.

Analyzing 2,789 actively managed mutual funds between 1979 and 2014, the researchers find that fund portfolios have become more liquid over time, largely as a result of becoming more diversified. Both components of diversification—balance and coverage—have risen sharply, especially since 2000. The level of coverage rose faster than the level of balance as mutual-fund managers poured ever more names into their portfolios.

The research captures the rise of closet indexing among active-mutual-fund managers, a phenomenon that may be caused by managers hewing toward the benchmark they are trying to outperform. While diversification has some benefits in terms of risk management and liquidity, the close resemblance of active portfolios to passive indexes might leave some investors wondering why they’re bothering to pay for active management given the ubiquitous availability of cheap, passive alternatives.

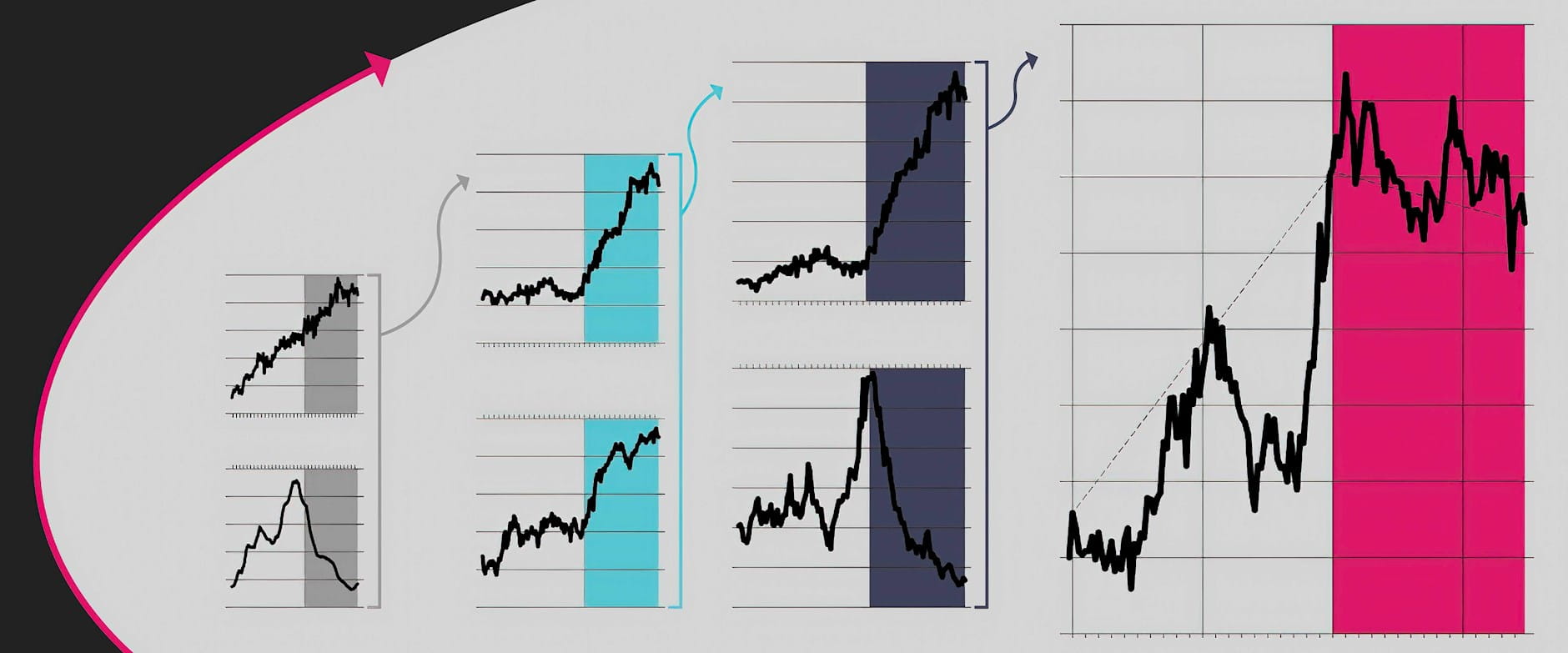

Liquidity of mutual funds’ stock portfolios

Investors should see lower trading costs with a mutual fund that has greater portfolio liquidity, which the researchers define as being more diversified and trading more-liquid stocks. This sequence of charts illustrates how they use a combination of custom portfolio characteristics to construct a measure of portfolio liquidity.

![]()

![]()

![]()

Mutual funds’ portfolio liquidity approximately doubled between 1980 and 2000, but it has been relatively stable since 2000, with the rise of diversification countering the drop in stock liquidity.

Lubos Pastor, Robert F. Stambaugh, and Lucian A. Taylor, “Fund Tradeoffs,” NBER working paper, December 2017.

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.