Douglas W. Diamond Says the Next Crisis Will Be Different

We can’t eliminate crises, but we can limit their severity.

Douglas W. Diamond Says the Next Crisis Will Be DifferentIn the US housing run-up, which peaked in 2006, banks allowed homeowners to borrow money with few conditions, issuing loans that required little documentation. The assumption was that if homeowners defaulted, rising housing prices would help lenders avoid losses.

In a boom, banks and bond markets make the same types of loans to companies, suggests research by Chicago Booth’s Douglas W. Diamond and Raghuram G. Rajan and University of North Carolina’s Yunzhi Hu, a recent Booth PhD graduate. Instead of no-document home loans, banks issue covenant-light corporate loans. These loans, and the willingness of banks to issue them, could make future busts longer and more painful.

We can’t eliminate crises, but we can limit their severity.

Douglas W. Diamond Says the Next Crisis Will Be DifferentDiamond, Hu, and Rajan start by asking why downturns are so severe and long. They reject the traditional explanation, that debt built up during a boom restricts investment. Instead, they build a model in which financing and leverage play a large part—and leverage is closely related to a concept the researchers term “cash flow pledgeability.”

“Pledgeability” refers to actions a company can take to make it easier to lend against its value—and enhance the ability of a lender to figure out what the company is worth. Some examples include ensuring accounting transparency, taking out patents rather than relying on the institutional knowledge of in-house scientists, and setting aside cash in an escrow account.

Sometimes banks are more willing to lend—or buyers, more willing to step in and buy a company from bankruptcy—if a company has high pledgeability. But there’s a downside for managers: pledgeability can make it easier to replace current management with outsiders.

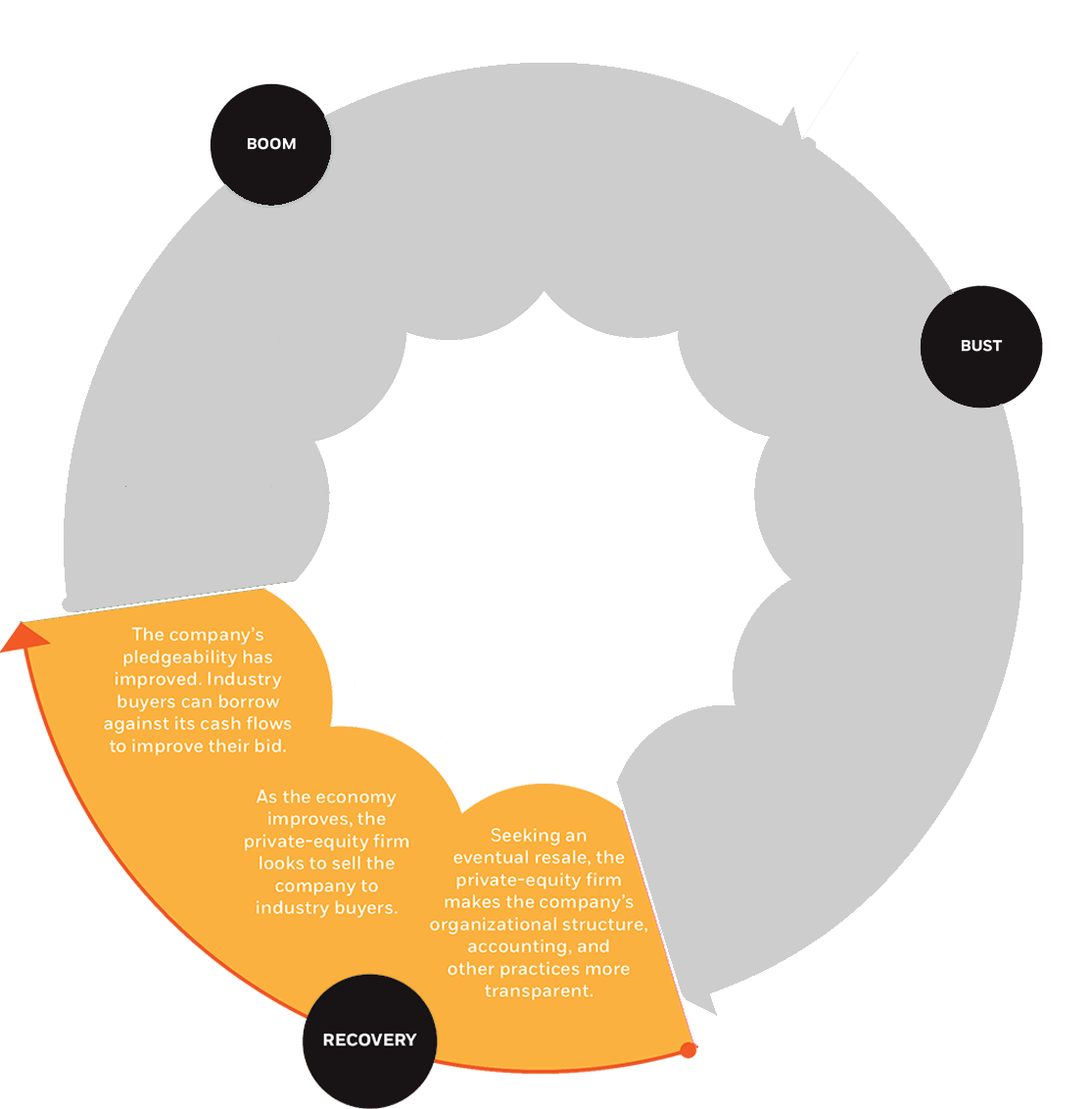

A company’s decision about ‘pledgeability’ feeds a cycle of booms and busts

Click the ![]() below to see how decisions about pledgeability can shape a company’s future and prolong recession.

below to see how decisions about pledgeability can shape a company’s future and prolong recession.

1 of 1

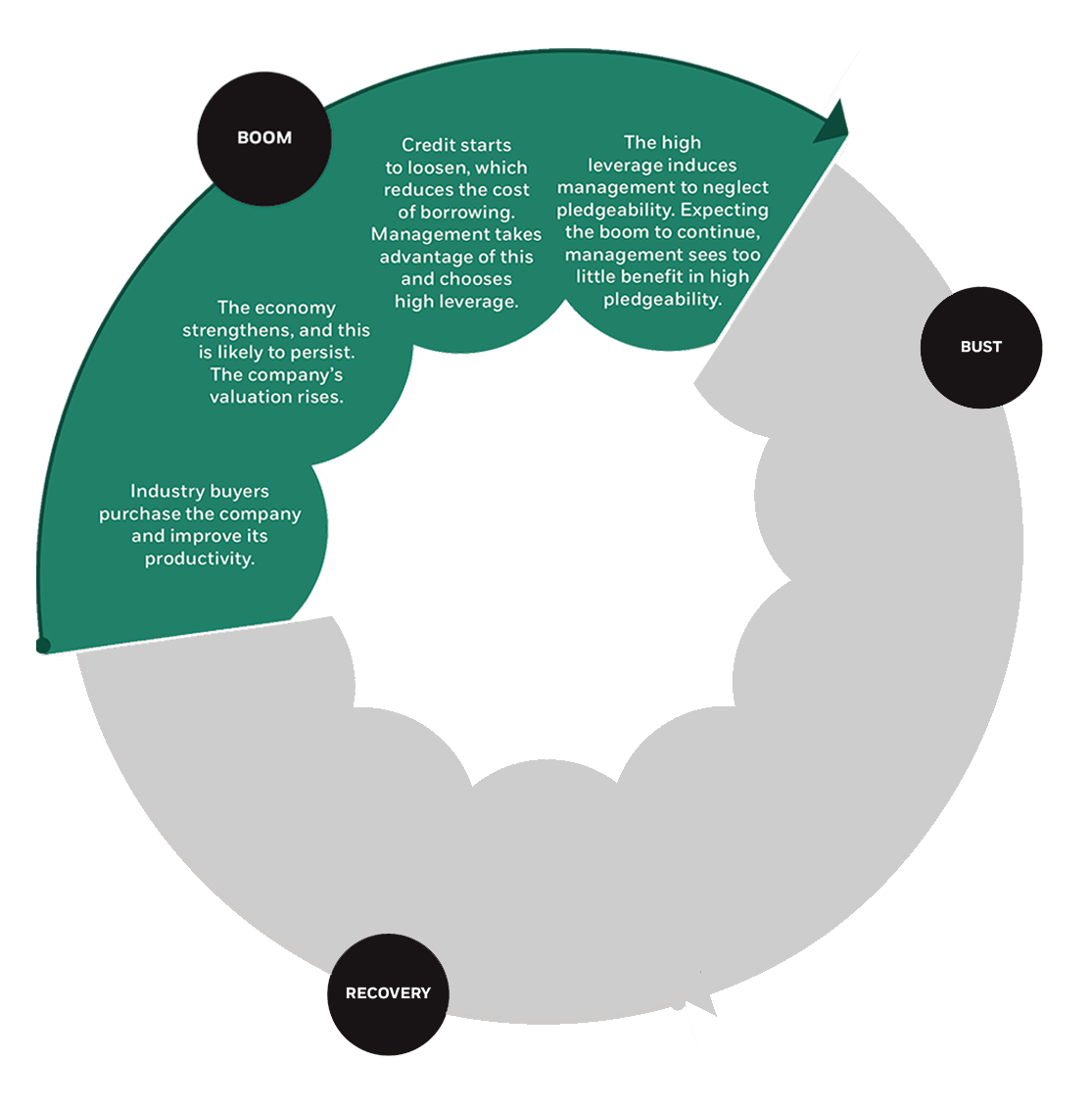

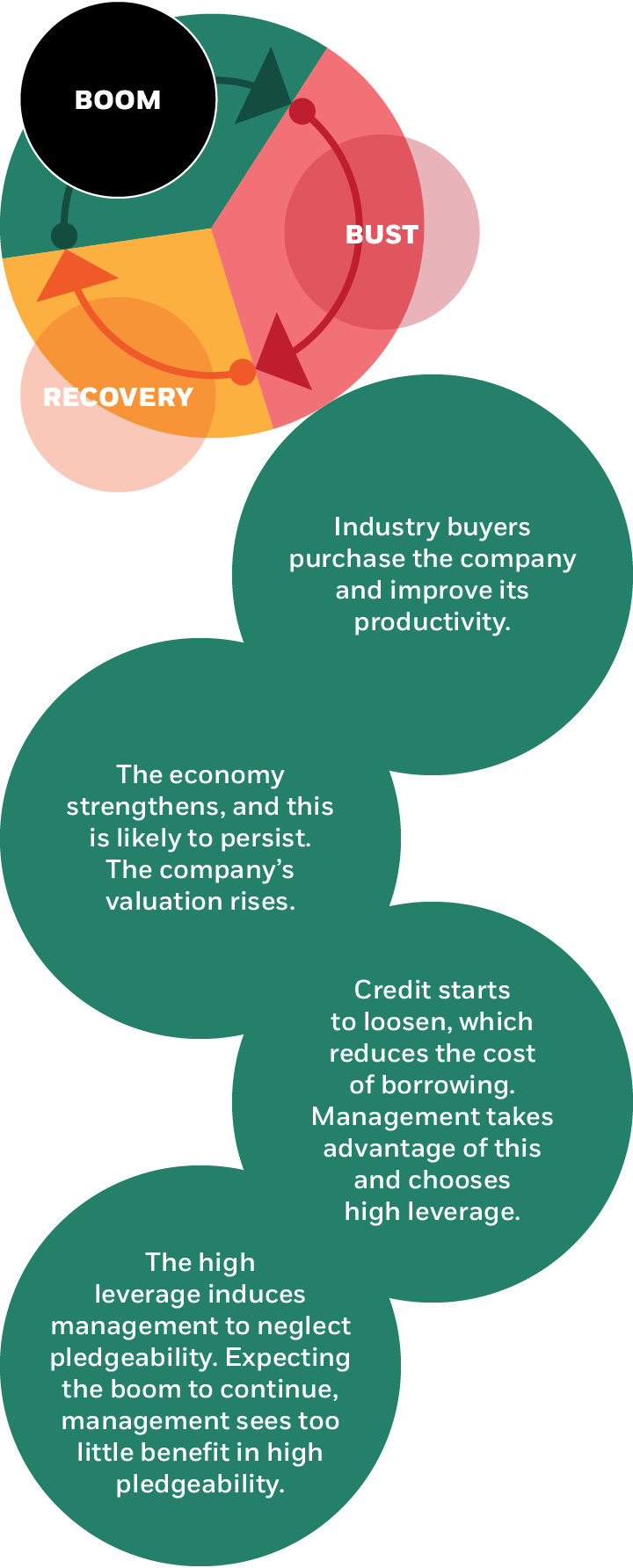

The researchers outline how demand for pledgeability varies with the economy, which leads to a cycle. When the economy is booming and shows no signs of slowing, banks are less concerned about pledgeability and are willing to do business with even opaque companies. In this case, banks issue more covenant-light loans.

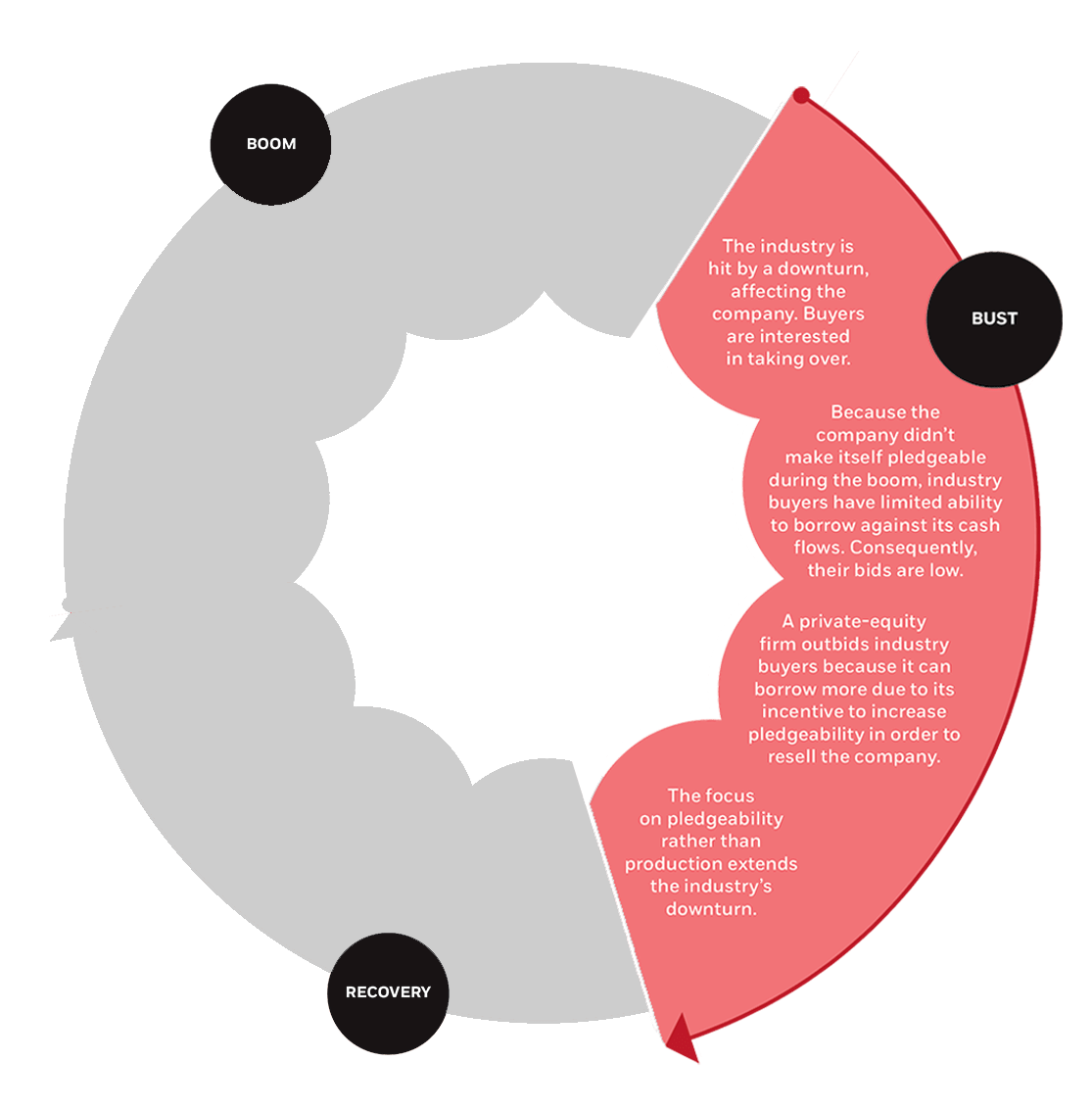

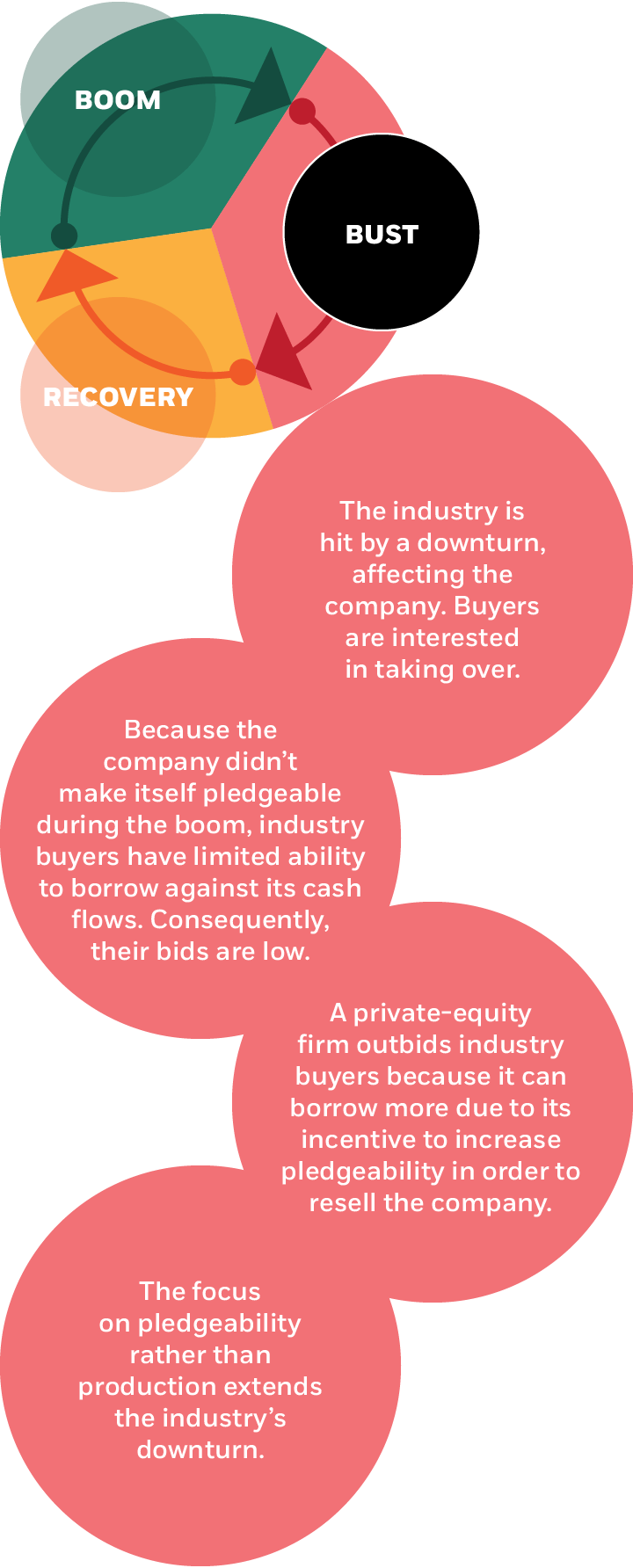

In a boom that may not continue, lenders may be somewhat concerned about pledgeability, and a company’s managers have to weigh the trade-offs involved. It is likely, however, that in such times, a company can still borrow more with high leverage and low pledgeability. And in a bust, lenders demand pledgeability and lower leverage, because the managers’ pledgeability decisions have large ramifications.

If a company has opted to be more pledgeable but goes bankrupt in a bust, its pledgeability could help it finance a sale to an industry insider who will run it— allowing a higher recovery to lenders in bankruptcy. If a company instead opted against pledgeability, industry insiders would have a tough time financing the sale, and the company might get bought up at a low price by outsiders who don’t know much about the industry but are better able to raise financing. Under them, productivity can fall, and this can make a downturn more painful.

However, “while industry outsiders have little ability to operate the asset themselves, this may be a virtue—outsiders have a strong incentive to improve cash flow pledgeability because they do not want to own the asset long term, but instead want to sell the asset back to industry insiders at a high price,” the researchers write. Thus, these outsiders, such as private-equity firms, can replace managers and improve pledgeability until they can flip the company for a profit. But eventually “the incentive to maintain cash flow pledgeability wanes once again,” the researchers write, “and the cycle resumes.”

Douglas W. Diamond, Yunzhi Hu, and Raghuram G. Rajan, “Pledgeability, Industry Liquidity, and Financing Cycles,” Working paper, December 2017.

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.