The oil giant’s listing on the Saudi stock exchange carries three considerable dangers.

- By

- December 05, 2019

- CBR - Finance

The oil giant’s listing on the Saudi stock exchange carries three considerable dangers.

It’s rare for a country’s fate to depend on the fortunes of a single company, but that is the case with Saudi Arabia and Aramco, the Saudi Arabian Oil Company, which is expected to list its shares in an initial public offering on the Saudi Arabian stock exchange in mid-December 2019.

On the face of it, this is an exciting moment for investors. The 80-year-old state company is the world’s most profitable, and potentially most highly valued corporation. Its listing is expected to be the world’s biggest IPO, surpassing the $25 billion raised by Alibaba in 2014. (All prices and values in this article are given in US dollars.) Aramco is widely thought to be well managed and well organized. Its principal product—oil—remains essential, even though oil’s preeminence is projected to end during this century. And Aramco has a reasonable strategy for navigating a fast-changing landscape: hedging bets with other oil producers while locking in long-term relationships with buyers.

But this will likely not be enough to persuade investors, especially Western investors, to buy in. First, oil companies no longer capture the imagination of investors. Second, a Saudi oil company comes with too much additional baggage. And what’s more, Aramco’s IPO is an anachronism: the time for sharing risk with foreign investors passed a decade or so ago.

Mohammed bin Salman is Saudi Arabia’s crown prince, the de facto ruler of the country, and the final arbiter of decisions at Aramco. MBS, as he’s commonly known, has repeatedly expressed his desire to list as much as 5 percent of Aramco’s 200 billion shares on Saudi Arabian and overseas financial markets at a valuation of $2 trillion.

The impetus for the Aramco IPO is best understood within the larger context of the political and socioeconomic challenges faced by Saudi Arabia. The country is dangerously dependent on oil: in 2018, the petroleum sector contributed 87 percent of the government’s budget, 90 percent of export earnings, and 45 percent of GDP.

MBS’s Vision 2030 plan aims to reduce this oil dependency, as well as Saudi Arabia’s citizens’ reliance on the state. The Aramco IPO is cast as a critical element of the plan, providing some of the financing necessary to diversify the Saudi economy through investments in manufacturing, high technology, entertainment, and tourism.

In November 2019, Aramco’s plans for a dual listing were thrown into disarray after its investment bankers revealed that Western investors were balking at purchasing shares in Aramco at a valuation of $2 trillion. Analysts at the big global banks came up with a wide range of valuations and, more fundamentally, identified key sources of uncertainty. Operating on the premise that oil prices will stay at or above $60 for the next five years, Goldman Sachs has valued Aramco at $1.6 trillion to $2.3 trillion. Reflecting a much wider range of possibilities, Bank of America has concluded that Aramco’s valuation could range from $1.22 trillion to $2.27 trillion.

Piqued at the underwhelming response of overseas investors, Aramco has shelved plans to list its shares overseas and intends to concentrate, for now, on a Saudi Arabian listing. Its current plan is to list up to 1.5 percent of its outstanding shares at a valuation of $1.5 trillion to $1.7 trillion. To boost demand, Aramco has “promised” investors (a share of) an annual $75 billion dividend for the next five years and zero-interest loans to finance share purchases, as well as a bonus share (for every 10 shares purchased) if they hold on to their shares for 180 days.

Aramco’s business strategy must be understood within the context of Saudi Arabia’s role in the Organization of the Petroleum Exporting Countries. The intergovernmental organization was established in 1960 to try to coordinate the petroleum policies of its members and ensure stable oil markets. Over time, Saudi Arabia has come to assume the unofficial mantle of OPEC’s leader.

In economics textbooks, OPEC is generally portrayed as a cartel whose principal objective is to sustain monopoly profits by reducing excessive competition among its members. The reality is more complex, since OPEC has always had to contend with many independent oil-and-gas-producing countries, most notably the United States and Russia.

Saudi Arabia has repeatedly emphasized that sky-high oil prices are not in OPEC’s interests, as they induce buyers to reduce oil use and to actively search for substitutes. As Ahmed Zaki Yamani, a former Saudi oil minister, is often credited with observing, “the stone age did not end because the world ran out of stones.” Consequently, Saudi Arabia has traditionally acted as the swing producer by increasing or decreasing its oil production to maintain “stable” prices and volumes.

But two megatrends are forcing Aramco to reevaluate its role as the swing producer. The first megatrend is the addition of new sources of supply of oil and gas from non-OPEC members. Because of innovations in hydraulic fracturing and horizontal drilling, there has been a five-fold increase in the production of shale gas in the US over the past decade, according to the US Energy Information Administration. In public, OPEC has clung to the view that shale-gas production has peaked, and that OPEC is well positioned to reassert its dominance. Yet shale-gas production has been increasing each year, and is not expected to peak until 2040.

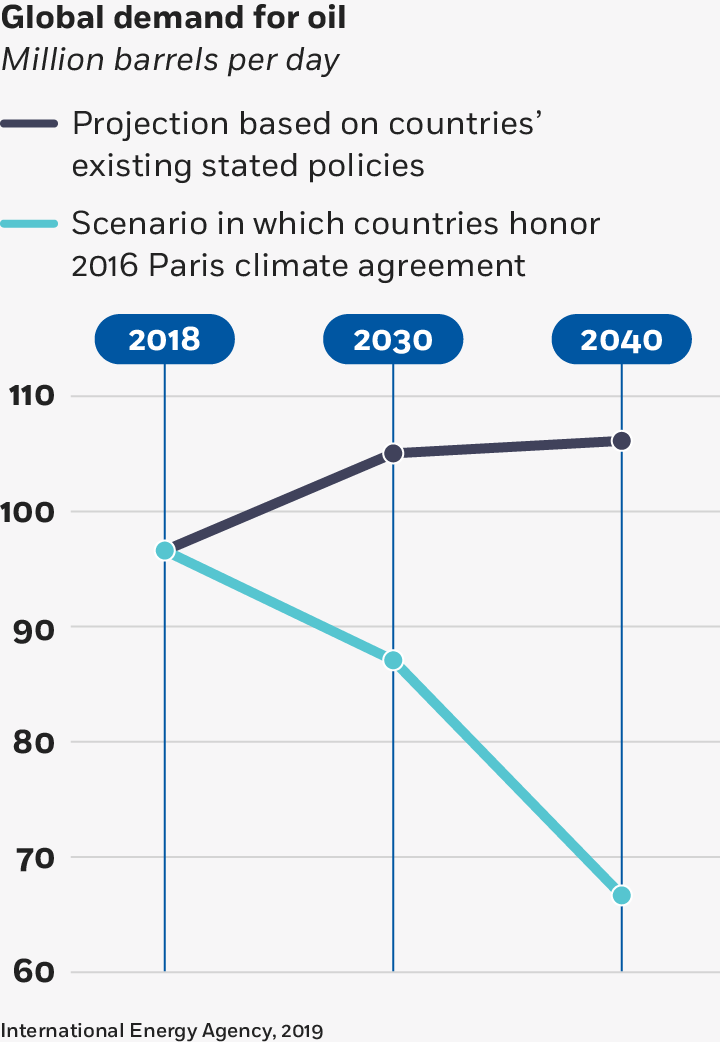

The result is that global oil demand is expected to grow more slowly than global supply over the next five years, according to the International Energy Agency, ratcheting up pressure on Saudi Arabia and other OPEC members to sustain their cooperation. According to my calculations, oil revenues account for more than 70 percent of export revenues for all 14 OPEC members, which means the incentives to defect from OPEC agreements are nontrivial.

The market for oil in coming decades will depend heavily upon how policy makers choose to address climate change.

The second megatrend is that public sentiment in the Western world toward fossil fuels has turned sharply negative. Storms, floods, fires, and droughts are now more incessant and harsh, and there is widespread acknowledgement that these phenomena are linked to fossil-fuel use. Changing weather patterns and global activism have put pressure on politicians in Western democracies to develop policies to address climate change. Given that many of the protests are led by young figures such as Greta Thunberg, such pressure is likely to increase in the coming decades.

For most of the 20th century, the primary fear was that the world would run out of oil sometime in the second half of this 21st century. Today, some experts expect the demand for oil to taper off before oil runs out. And though there is a wide variation in opinion on when oil demand will begin to decline, there is a consensus that the substitution away from oil will happen within the next four decades. The most aggressive forecasts have oil demand declining by the late 2020s; the most conservative estimates expect oil demand to peak in the early 2050s.

These trends are showing up first in the transport sector, which currently accounts for about 60 percent of oil consumption, according to BloombergNEF. While electric engines are now proven to work, their cost compared to traditional engines depends on the price of lithium-ion batteries, which has fallen dramatically from a high of $1,160 per kWh in 2010 to a low of $176 per kWh in 2018. Most experts expect the tipping point for electric cars to come when lithium-ion batteries hit a price of about $100 per kWh. The big automobile companies are preparing: BMW, Daimler, and Volkswagen all expect at least 15 percent of their sales revenues in 2025 to come from electric cars.

Oil’s strongest growth opportunity is in petrochemicals. It is still an essential ingredient in the production of clothing, electronics, fertilizer, and plastics. But even here, the tide is beginning to turn, as the world’s biggest companies in these sectors commit to exploring alternatives to fossil fuels.

These trends mean that Aramco’s dynamic optimization problem has changed. A decade ago, the company might have viewed its time frame for extracting its 260 billion barrels of oil reserves as being as much as 100 years. Today, its decision makers likely see the time frame as less than 50 years.

Recognizing these tectonic shifts, Aramco has embarked on a series of deals to build long-term relationships with oil-hungry countries such as India and China, and to diversify its portfolio. Since 2015, Aramco has taken equity investments and entered into joint ventures with partners in China, India, Malaysia, and South Korea. In April 2019, Aramco took a 70 percent stake in SABIC, the Saudi company that is the world’s fourth-largest petrochemical business, signaling its intent to expand downstream. In many of these deals, Aramco guarantees long-term crude-oil supplies, thereby hedging its bets with OPEC.

Prospective investors are weighing the rewards and risks of investing in Aramco. On the positive side of the ledger, Aramco’s advantages in extracting oil (at a reputed cost of $3 per barrel) and its scale of operations are unmatched. Its EBITDA (earnings before interest, taxes, depreciation, and amortization) margin of 63 percent is twice as big as its largest rival, Russia’s Gazprom, and its proven oil reserves of 260 billion barrels of oil are more than three times greater than the reserves of the next five largest oil companies combined.

The carrot that Aramco is dangling—a share of a promised dividend payment of $75 billion—is attractive in today’s low-interest setting. And while the shares may not gain value, the size of the Aramco listing means it will be included in the MSCI (Morgan Stanley Capital International) Emerging Markets Index, which should ensure a stable source of demand from passive investment funds.

But Aramco also poses three distinct sources of risk for investors. The first is a corporate-governance risk. While Aramco claims that it has a “rule-based relationship” with the Saudi government and a history of “operating independently,” most experts agree that on the issues that matter, Aramco would align itself with the interests of its masters over those of its minority shareholders. All consequential decisions at Aramco will have to be approved by MBS. Potential investors should be particularly concerned about the promised $75 billion dividend. The temptation to stop paying dividends in periods of crisis (for Saudi Arabia or Aramco) could prove irresistible. Standard and Poor’s estimates that Saudi Arabia’s 2018 fiscal deficit of approximately $50 billion will grow steadily over the next five years because welfare spending and military expenditures will continue to expand rapidly. The International Monetary Fund reports that Saudi Arabia’s budget is balanced when oil prices are $85. As I write this, the price of Brent crude today lingers more than $20 per barrel below that.

Elite companies’ methodologies tend to share some common traits.

How to Develop a Superstar Strategy

A case study in what can happen to a conglomerate that fails to adapt quickly when its success falters.

Three Strategy Lessons from GE’s DeclineThe second source of risk for investors is the potential that the House of Saud loses control of its oil fields. While this may seem like a low-probability event, in the Middle East, regime change cannot be ruled out. The House of Saud has many enemies internally and externally. Externally, its principal rival is Iran, with which it has fought (and is fighting) proxy wars in Yemen, Iraq, Syria, and Lebanon. The Iranian nuclear weapons program is as much of a threat to Saudi Arabia as it is to Israel; the US embargo on Iran was likely cheered as loudly in Riyadh as it was in Tel Aviv.

The House of Saud also faces many internal enemies. Over the years, a number of violent extremist groups have turned their ire on the Saudi royal family. Al-Qaeda and the Islamic State are thought to have a presence in Saudi Arabia. In 2009, a suicide bomber detonated his bomb in the presence of Prince Mohammed bin Nayef, the Saudi minister of the interior, who survived. By many accounts, the Saudi security forces have put down enemies ruthlessly. Investors who bet on Aramco are effectively betting that the House of Saud will retain operational control over Saudi Arabia and its oil fields.

The third source of risk, a tapering off in oil demand, will likely exert an influence on Aramco’s prospects in the years to come. If sustainability objectives, such as the UN Intergovernmental Panel on Climate Change’s goal of limiting global warming to 1.5°C, drastically reduce global demand for oil, the economic and political consequences for Saudi Arabia could be dire.

Would investors view the IPO differently if they had the chance to invest not in Aramco but Equinor, the state-owned oil company of Norway? More than likely, yes. Corporate-governance concerns would not disappear, but they would be considerably muted. So would the prospect of expropriation via a forced change in ownership and control.

But the risk that would not disappear is the possibility that the demand for oil may fall dramatically in the coming decades. In decades past, investors might have jumped at the chance, their concerns about corporate governance overshadowed by their fear of missing out. Some investors will still be tempted. But for many, the Aramco IPO will be the moment they turned down the opportunity to give financial support to a regime managing a debt-fueled economy, and to invest in an industry in long-term decline.

Ram Shivakumar is adjunct professor of economics and strategy at Chicago Booth.

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.