Alex Fine

Has the World Gone Crypto Crazy?

What you need to know about Bitcoin, blockchain, and cryptocurrency

- By

- May 11, 2018

- CBR - Finance

In the past several months, I have been bombarded with students working on crypto projects. Two of our Global New Venture Challenge teams plan to issue cryptocurrency and use initial coin offerings (ICOs) to raise money. Our undergraduates organized a conference on crypto, and with little advance warning and almost no marketing, the house was packed to the gills. Entrepreneurs are coming out of the woodwork with new blockchain applications. What is crypto and blockchain, and is Bitcoin the next currency or a scam? When I set out to educate myself, I discovered a fascinating world of technology disruption and 21st-century finance in which supporters and detractors abound.

Plenty has been written, and is being written, about cryptocurrencies, Bitcoin, and blockchain. CBR had two such articles in its Spring 2018 issue: “The Bitcoin market isn’t irrational” and “The good and bad of blockchain.” I’ve noticed that many people are mixing and matching crypto-related terms with abandon, which has confused the heck out of me and most people I know, so this essay is intended as something of a primer that I hope is helpful. But I must start with a disclaimer: I am not a blockchain technology specialist, a financial industry lawyer, or a cryptocurrency expert. I’m just a person who would rather live in this brave new world with some knowledge than ignore the crypto craze and hope it just goes away.

Lesson 1: Bitcoin is, in fact, money.

Typically, the word “currency” describes what the crypto crowd calls fiat money—paper currency made legal tender by the fiat of a government. Money is nothing more than a societal agreement that the currency we use—the US dollar, for example—has value, because a government backs the currency. As the government in question is the United States, that government backing is considered strong assurance that the money will retain an agreed-on value as people exchange it for goods and services.

But sometimes that societal agreement fails. National Public Radio’s Planet Money podcast produced an outstanding episode in 2010 called “How Fake Money Saved Brazil,” which chronicled a period in the 1980s when Brazilians lost faith in their currency, the cruzeiro. Rampant inflation destroyed the value of cruzeiros, making prices for basic items including food completely unpredictable and outrageously high. Some economists decided that the way to address the runaway inflation was to create a new currency—a fake one—which they called the unit of real value (URV). The government declared that all prices would be listed in URVs, and wages and taxes would be paid in URVs. The fake currency stayed stable while the number of cruzeiros per URV fluctuated. Gradually, people started to think in terms of URVs rather than cruzeiros. They began to trust that a quart of milk that cost one URV on one day would still cost one URV the next month. Eventually, the URV replaced the cruzeiro as the “real” currency in Brazil and was renamed the real (pronounced “hey-al”). Inflation settled down and a long period of growth for the Brazilian economy followed.

What does this have to do with cryptocurrency? The first cryptocurrency was Bitcoin, and it, in fact, similarly represents an abstract unit of value that can be exchanged for goods and services. That’s true predominantly in the virtual world right now—you can use bitcoins to pay for travel at Expedia, home goods at Overstock, technology at Microsoft, even satellite TV at Dish Network—but increasingly in the offline world as well. But a government isn’t backing Bitcoin and calling it legal tender—instead, a combination of technology and the societal agreement that has grown up around that technology gives Bitcoin its value.

Blockchain, being a new technology, is proving itself not quite ready for prime time.

The US government can issue dollars to help banks meet demand for cash, or to allow the government to buy back Treasury bonds. Simply speaking, the government manages the supply of currency to keep dollars valuable and liquid while avoiding the kind of inflation that troubled Brazil in the 1980s. The technology embedded in Bitcoin regulates how new bitcoins are created, owned, and traded and underpins Bitcoin’s value as a useful currency—the way government fiat does for the dollar. For example, Bitcoin’s creator set a permanent 21-million-bitcoin limit to create scarcity, theoretically increasing the value of the asset. Nearly 17 million bitcoins are circulating so far. The coins are created in a process called mining, by people who allow the Bitcoin network to use processing power on their computers to perform mathematical tasks and to store the database of bitcoin owners. A miner is compensated when this process generates a new bitcoin.

Crypto’s volatility

Bitcoin, Ether, and more than 1,500 other cryptocurrencies have fueled the global market’s dramatic ups and downs.

When a bitcoin is created, data about its existence and its owner are stored on a ledger that lives, in multiple copies, on many miners’ computers—a distributed ledger, in Bitcoin parlance. The technology that enables the ledger is blockchain, which uses math and processing power to encrypt information about each bitcoin and its ownership. It then batches up that information with other bitcoin transactions happening at the same time into a block and connects that block to every other transaction block in a chain. This creates for every transaction a permanent record that can’t be altered without changing the blocks before and after it in the chain of records. To trade a bitcoin, its owner needs to notify the miners who manage the chain about the trade, and their computers will verify and process the information about the current owner, new owner, time of the transfer, and amount exchanged—using complex math problems embedded in the blockchain technology. Finally, the miners will add the transaction to the distributed ledger on all the other miners’ computers. That level of distribution and connectedness makes the ledger secure.

The fact that the ledger is distributed rather than controlled by a central organization is what made Bitcoin so appealing to early users for online transactions. Payments don’t have to go through any banking system, aren’t tied to any specific offline currency or government, and are both anonymous and secure. This quickly made Bitcoin the de facto currency of the so-called dark web. According to Coinbase, a leading information service focused on cryptocurrencies, a mere five years after Bitcoin was introduced in 2009, transactions on six dark-web marketplaces topped $650,000 a day. Then the mass market adopted Bitcoin, increasing transaction fees and slowing down transaction speeds, and regulators woke up to this new currency, threatening the anonymity of the transactions. New cryptocurrencies such as Litecoin and Dash emerged to dilute Bitcoin’s hold on the underworld.

Lesson 2: Blockchain is more than a tool to create currency.

While Bitcoin was establishing itself as a useful currency, technologists discovered the power of the blockchain distributed-ledger technology. A financial transaction is like any other transaction—an action based on data and rules. Developers began to create blockchain systems for uses other than pure monetary exchange. The second largest cryptocurrency, Ethereum, isn’t a currency in the monetary sense. It is, instead, a platform on which developers can build new internet applications that take advantage of the security and decentralized aspects of blockchain technology. Already more than 500 gaming, messaging, social networking, news, and business applications are being offered as distributed applications, or dapps, built on the Ethereum infrastructure. In this architecture, the coins or “tokens” are not intended as money to buy and sell things. Instead, each token grants a person the right to use some aspect of the app—for example, a token can allow you to play a game in an online arcade. Rather than buy a subscription or license for the software, users buy crypto tokens that allow them to execute transactions in the applications, essentially prepaying for using the system.

It is blockchain, rather than Bitcoin, that has corporate giants including Walmart, Maersk, and FedEx investing in a new generation of supply-chain solutions. Meanwhile, Bank of America, Mastercard, Fidelity, and IBM are the top four blockchain patent owners in the US.

Lesson 3: The world has gone crypto crazy.

Bitcoin has real value as a currency. Blockchain technology has the potential to enable new systems that could create enormous value. In that case, why are there so many detractors declaring crypto to be the next bubble, or even worse, a scam? The answer is that there are problems in the world of crypto, including both the blockchain-technology mania and the cryptocurrency boom.

Power hungry

The amount of electricity required to process bitcoin transactions climbs every day.

Blockchain, being a new technology, is proving itself not quite ready for prime time. Already, the original blockchain system is suffering scale issues. The network can process only about seven transactions per second, which is relatively slow. These transactions require so much processing power that Digiconomist estimates the current Bitcoin network is using enough electricity every day to power the entire country of Greece. That has set off alarm bells with environmentalists. It will take time for the technology to mature into a widely adopted, scalable infrastructure for new systems.

On the currency front, the problems are worse. There are now over 1,500 types of crypto coin and token. Bitcoin has a technology architecture that creates new bitcoins one by one, according to specific rules and through intensive computer processing, but other cryptocurrencies come to market through ICOs. In these, companies create their own tokens and simply sell them. Why would anyone buy a brand-new cryptocurrency that has neither a track record nor an established market value? Theoretically, the value of the token represents what you can do with it in the blockchain network issuing it. For example, to use an application built on the Ethereum platform, you buy tokens that allow you to access and use the Ethereum-based dapp. But ICOs are frequently offered before there is any software ready to use—and sometimes with nothing at all to drive value for the tokens.

According to its creator, Dogecoin was started in 2013 as a joke, a parody of the many cryptocurrencies appearing in the market on the heels of Bitcoin. Buying Dogecoin cheaply and joining the community became an affordable way to get educated about cryptocurrency, and until April 2017, the market value of all Dogecoin was only $25 million. Then the market was hijacked by speculators and uninformed crypto investors, and its market cap soared to $2 billion this past January—for a currency that began as a joke! Dentacoin markets itself as the blockchain solution for the dental industry. With its website promising a test launch in the fourth quarter of 2018 and integration with health-care databases in 2019, Dentacoin also saw a market cap that topped $2 billion in January. By March, it had come back down to $91 million, still a hefty price tag for a token with no current use. In the underregulated Wild West of crypto, self-proclaimed pump-and-dump groups brazenly advertise their membership opportunities. Get in, buy the designated cryptocurrency at a set time, then sell when the market thinks this is the next Bitcoin and jumps in.

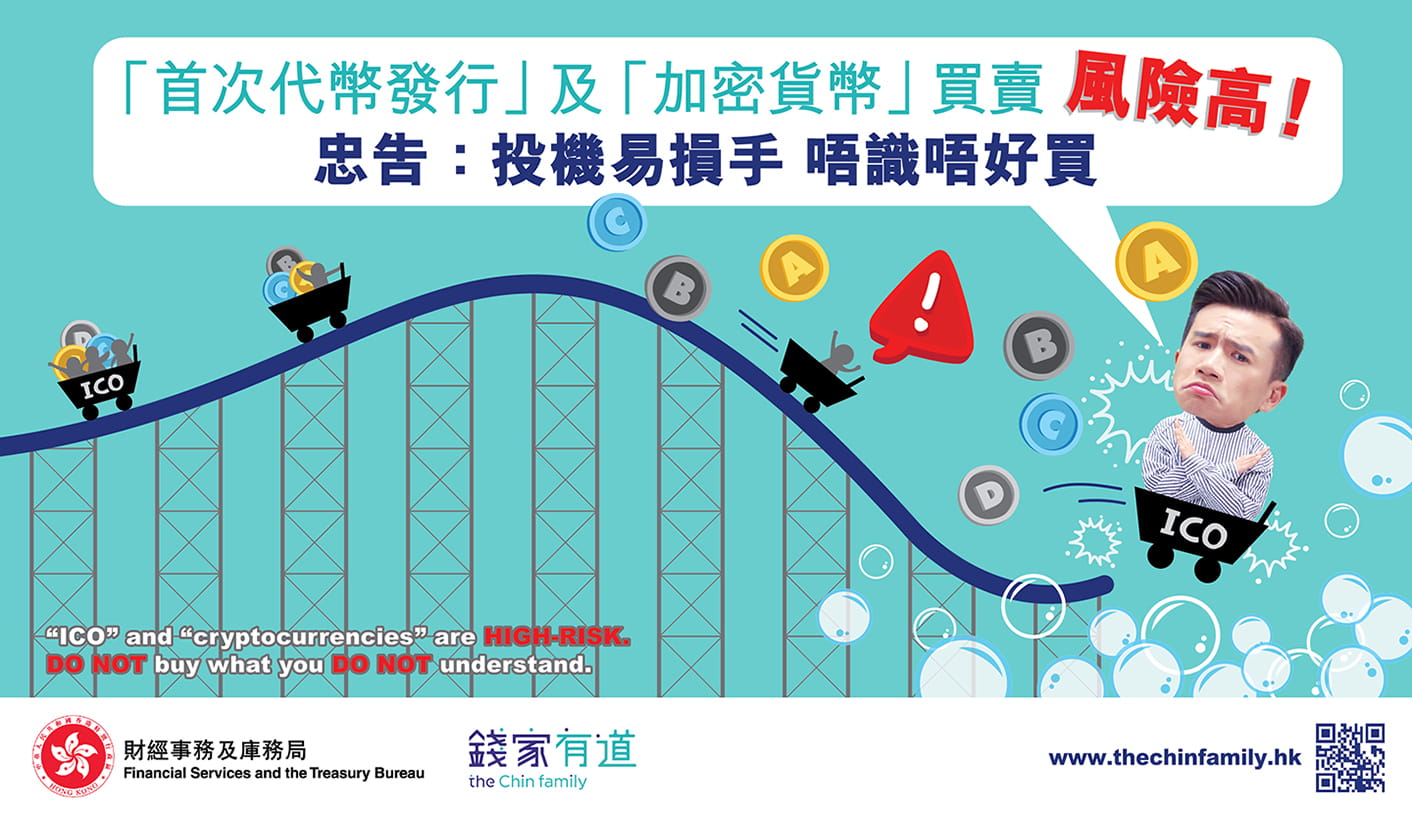

In Hong Kong, the government placed an ad in the subway system warning its citizens that ICOs are risky. Photo courtesy of Investor Education Centre

In fact, according to ICOdata.io, a data-collection and ICO-rating company, 881 start-ups raised more than $6 billion in 2017 using ICOs, and by the beginning of April of this year, more than 500 companies had already raised more than $3 billion. This funding is not subject to the due diligence of angel or VC money; nor is it regulated, as is the emerging peer-to-peer equity crowdfunding market. As a result, the ICO market is rife with scams and failures. Bitcoin.com, a cryptocurrency news site, reports that nearly 60 percent of the ICOs offered in 2017 have already failed or are in the process of disappearing.

On April 10, 2018, CoinMarketCap, which tracks the value of each of the 1,550 plus cryptocurrencies, showed the total crypto world as having a market cap of more than $264 billion. This is up more than 1,000 percent from $26 billion at the beginning of April 2017, but is less than 30 percent of its high of $813 billion in January 2018. This kind of volatility reduces crypto’s value as a currency the same way runaway inflation killed the cruzeiro. And how does the investor sort the wheat from the chaff in choosing the tokens that will be useful and valuable in the future? Most people won’t be able to. China has already banned ICOs, and in Hong Kong, the government has placed an ad in the subway system warning its citizens to stay away from ICOs.

My take after all this? The advice of the Hong Kong government is wise. By all means, if you need to do business across borders with unknown parties and Bitcoin is the right way to proceed, buy bitcoins. If you want to own and breed crypto-kitties, or need a secure email system, or want to use a smart-contracts application that uses the Ethereum platform, buy ether tokens. But if you think cryptocurrency is a surefire get-rich-quick scheme, buyer beware.

Waverly Deutsch is clinical professor and academic director of university-wide entrepreneurship content at Chicago Booth.

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.